Central Africa's Path Forward: Regional Digital Cooperation

~10 min read

Nestled in the center of the world’s fastest-growing continent, the region of Central Africa is at a juncture between a fractured past and a potentially integrated future. The Central African Economic and Monetary Community, otherwise known as CEMAC, comprises six countries - Cameroon, Chad, Equatorial Guinea, the Republic of Congo, Gabon, and the Central African Republic - and is home to a population of over 50 million. The region’s economy is dominated by the oil sector, which makes up 80 percent of exports and 75 percent of its income, leaving the region quite vulnerable to fluctuations in international oil prices. The recent downgrade of all CEMAC member countries made the region’s economic outlook relatively delicate. It’s against this backdrop that digitization could prove game-changing – for inclusion, entrepreneurship, and regional coherence -- to the potential benefit of millions of Central Africans.

By the end of 2019, overall growth across the region was a steady 2.5 percent; the IMF concluded that the economic and financial situation of CEMAC had marginally improved, but not fully recovered from the oil price collapse in 2014. Prior to the COVID pandemic, 2020 projections of GDP growth were promising, if the region was able to successfully implement macroeconomic reforms and diversify its exports. But both historically and today, Central Africa is one of the least integrated economic regions and suffers from high poverty rates, political instability and a governance and infrastructural deficit.

The increased use of technology in the region has resulted in an increase in digital services, particularly in the financial sector, introducing an opportunity for fintech innovation in the region. Regional integration, however, has been seen as a necessary step to reduce the fragility of its member states. The Africa Continental Free Trade Agreement was expected to achieve this by offering cross-border trade opportunities to promote digital transformation and economic diversification, but since its recent postponement as a result of COVID, CEMAC is left to its own devices to take steps toward regional harmonization. With sufficient backing, could increased digitization support regional integration, and thereby provide an alternative pathway to growth?

Continent, Region, And Country

Central Africa falls far behind other African Regional Economic Communities (RECs) in terms of both regional integration and economic development. CEMAC has long received strong recommendations from international institutions and investors to further integrate its financial services sector in order to drive innovation and growth.

If growth is the goal, financial inclusion could hold the key. Studies show that financial openness and inclusivity are directly correlated with economic growth. Regional financial integration can potentially address challenges that smaller, more fragmented African countries, like those that make up CEMAC, face. For example, consolidating financial systems tend to boost competition and innovation, improve financial infrastructure, and reduce technological and operational inefficiencies that often plague emerging market financial institutions. When the European Union was created, the resulting expansion of financial flows across borders and financial services integration were essential drivers for European member states’ monetary growth, resulting in positive contributions to GDP across the board, as well as other economic metrics. As explored in a previous Mondato Insight on the West African Eco Currency, the model of regional monetary integration has become increasingly popular, and has been replicated in West Africa as well, though the effort was recently delayed up to five years due to the pandemic.

Regional collaboration and harmonization of regulatory frameworks, particularly for fintech, is an essential component in attracting competition in the financial services sector and innovation among its service providers. And though there is consensus that lifting trade and regulatory barriers leads to healthier systems and economics, there is continued debate on the best approach to regional integration. Both West and Southern African RECs have experienced strong trade expansion and above-average performance as a result of regional cross-border financial integration. And like its neighboring blocs, CEMAC is in the process of advancing its efforts towards market liberalization, particularly in its financial services sector.

Though financial services liberalization leads to cost and other efficiencies, in the case of emerging markets, and Africa in particular, total market liberalization is not categorically believed to be the most successful approach. While critics of regional blocs believe that preferential regional trade may be encouraged at the expense of global trade, some level of protectionism can mitigate foreign exchange constraints suffered by smaller economies by fostering and protecting local ecosystems and their businesses.

Potential Upsides

Like other trade blocs, CEMAC countries utilize a single currency. The CFA Franc, sometimes referred to as XAF, is regulated by an independent monetary authority, the Bank of Central African States (BEAC). But as of 2018, CEMAC’s financial integration was still classified as underdeveloped, with its bank-led financial sector only scratching the surface of its potential. But according to the IMF, there has been significant progress in the region’s banking regulation like supportive policies to build regional reserves and ensure financial sector stability, as well as welcoming a stronger, more risk-based supervision of banks.

CEMAC’s financial ecosystem is dominated by mostly foreign-owned banks. The depth of this banking sector is limited, accounting for only 26.3 percent of GDP. Lack of financial infrastructure makes it difficult to deepen access to services. Density of branches in the region is approximately a hundred times lower than developed countries like Germany or Canada, and when it comes to financial inclusion, CEMAC’s figures are particularly low, even compared with the rest of Sub-Saharan Africa. Less than 15 percent of the adult population in CEMAC countries has a bank account. As part of the regional integration agenda, BEAC introduced a regional switch called the Interbank Electronic Banking Group of Central Africa (GIMAC) in 2015 to enable bank transfers within CEMAC. In 2018, GIMAC was comprised of 56 companies across CEMAC; membership, until recently, was limited to traditional banks and micro-finance institutions (MFIs).

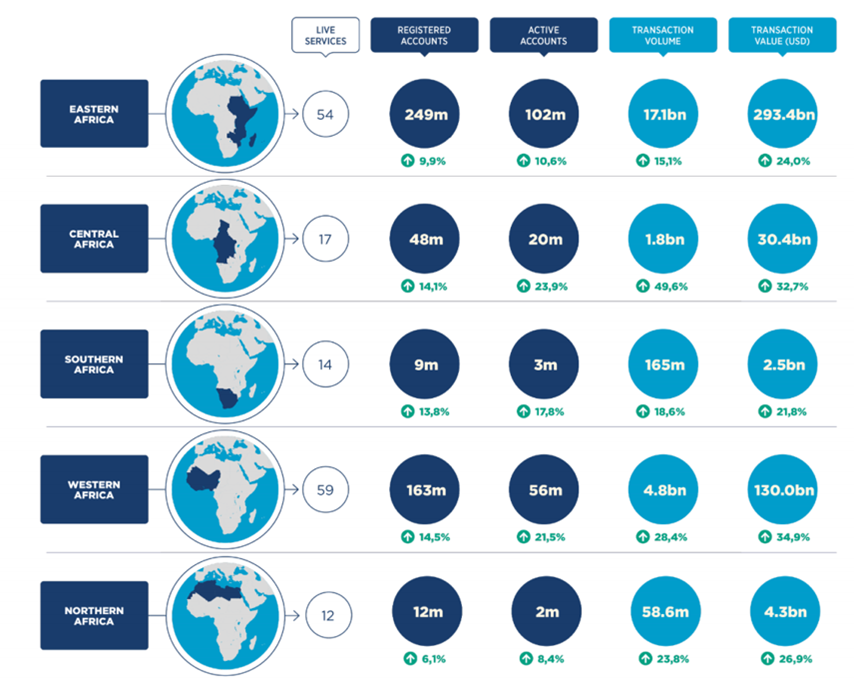

The telecoms sector, like its financial services brethren, is also dominated by foreign firms (MTN, Orange, Airtel), but has enjoyed more extensive penetration. 41 percent of the region’s inhabitants subscribed to a mobile account in 2019, and smartphone adoption reached 39 percent, making it ripe territory for mobile money. So it’s no surprise that mobile money has been on the rise with the region, representing 10 percent of registered mobile money accounts across Sub-Saharan, primarily led by Cameroon and Congo, and the number of accounts growing by 100 percent since 2016. In 2018, electronic transactions doubled, 99 percent of which were sent via mobile money.

Source: GSMA State of the Mobile Money Industry in Africa, 2019

Perhaps in recognition of the need to introduce a structured regulatory framework for mobile money transactions, BEAC announced its intention in 2018 to extend cross-border transaction permission to mobile money providers, alongside financial institutions and MFIs, through the existing GIMAC platform. Transactions between a bank and a mobile money wallet will now be authorized, though still blocked outside of CEMAC. The move is intended to introduce an element of regional interoperability, as well as lower transactions fees between countries to encourage trade. Abbas Mahamat Tolli, Governor of BEAC, announced in April that “mobile money interoperability was now effective within CEMAC”, and that it will “revolutionize the payment system in the region.”

GIMAC’s new platform is seen as a major step forward, since studies show that interoperable payments systems are a cornerstone to supporting digital financial transformation. Prior to the regulation, cross-border transactions required significant participation and formal partnerships. By inviting new players to participate in the digital finance ecosystem, independent from a traditional financial institution, there is hope for greater digital transformation and economic opportunities. But beyond person-to-person (P2P) transactions, banks still own the market on advanced financial services like credit and savings, potentially limiting the avenues of industry digitization.

Currently past its pilot phase and beginning commercial phase, the GIMAC interoperable platform confirmed participation from over fourteen financial institutions and mobile money operators within CEMAC, and has been continually welcoming new participants each month, all of whom will be required to use the GIMAC rails for transfers. While the headline of regional liberalization may hold true within CEMAC, transactions from outside continue to be closely controlled and restricted, with routine business and P2P transactions subject to increasingly restrictive regulations, even with neighboring African countries. In March, BEAC published new regulations further limiting transactions and account opening of residents outside the CEMAC zone, citing foreign exchange shortages as the culprit. This presents meaningful trade barriers between neighboring countries with larger economies, like Nigeria and the Democratic Republic of Congo.

In conjunction with the launch of GIMAC’s interoperable platform, a new regulation was issued introducing a Payment Service Provider (PSP) license that permits non-financial institutions to tap into GIMAC’s system for P2P transactions, in hopes of driving digital payment growth and lowering transaction fees for regional remittances.

But the number of potential participants may be limited to bigger businesses since the PSP license comes with a hefty capital requirement of US$850,000, though stakeholders believe smaller players will still benefit from GIMAC’s system. “Allowing payment aggregators and other smaller fintechs to leverage telco and bank distribution networks through GIMAC, without individual integrations with multiple players, will be a gamechanger,” according to Marcel Tchoulegheu, a Project Manager for ICT, Digital & Mobile Financial Services at MTN Cameroon.

It appears that CEMAC is flirting with a mixed-model approach to inclusive finance and regulatory reforms. On the one hand, inviting mobile money into the financial services infrastructure, and on the other, keeping those outside of CEMAC at arm’s length. It is yet to be seen whether this will successfully, or adequately, encourage digitization and innovation. And the potential gains that are found may potentially be unevenly distributed. Cameroon, CEMAC’s leading economy, already represents the majority of GIMAC members, as well as digital finance activity.

Cameroon Leading The Way

Home to more than half of CEMAC’s population, with the largest GDP in the region, Cameroon is often viewed as the economic leader of Central Africa. With the highest literacy rates in Africa, at 77 percent, it may hold the most regional promise for meaningful digital financial services penetration.

Compared to the rest of CEMAC, and even relative to other markets in Sub-Saharan Africa, Cameroon has enjoyed impressive mobile money penetration. Joseph Abena, Head of Marketing, Communication and Innovation at Orange Money said Cameroon has the highest rate of mobile money subscribers compared to mobile subscribers across its African markets. He attributes this to the strict, long-standing Know Your Customer (KYC) requirements in the country, which made mobile money sign-ups and onboarding easier. Additionally, early partnerships with the main electricity utility provider, ENEO, the state rail company, CAMRAIL, and Total’s fuel stations drove significant growth by quickly and visibly plotting a nationwide distribution network. Other common use cases aside from airtime top-up include bill payments and subscriptions, school fees and rent payments.

Last year, Minette Libom Li Likeng, the Minister of Posts and Telecommunications (Minpostel), announced the government’s goal to increase digitization and access to financial services across Cameroon. The Cameroonian government has been busy trying to support its digital economy, and in February created a start-up incubator for ICT-focused projects. Just following the ICT center announcement, the Ministry also announced the inauguration of a national payment switch. And the country’s various digitization were only expedited by COVID. The Minister launched a virtual hackathon, as well as a digital training course, to encourage Cameroonians to “propose ideas and concrete digital solutions that can enable Cameroon to manage the crisis caused by COVID.” She has also been quite vocal about the importance of producing domestic digital solutions to integrate into health practices. Though some initiatives implemented by Minpostel under the umbrella of ‘innovation’ have been met with criticism. One such effort is the recent introduction of an import tax on phones and tablets, aimed at optimizing customs revenue, but in turn, creating additional barriers to digitization.

Cameroon is investing in its digital skills significantly more than other markets, which is helping to build tech businesses within the country. Few of the existing payment service providers and aggregators in Cameroon are currently active in other CEMAC markets, with the exception of money transfer operators (MTOs) like WorldRemit, Western Union and MoneyGram. Imminent financial integration into the rest of CEMAC may incentivize companies to explore market expansion, or perhaps attract new players to invest in Cameroon, where access to CEMAC markets that may not justify their own business case is now more fluid.

Future Moves

CEMAC is employing a hybrid model of regulatory reform and protectionism, putting its economic liberalization on a tight leash. Public sector stakeholders, both in local governments and among regional representation, recognize that digital transformation and some element of openness are required to achieve more sustainable economic growth and diversification, or at minimum, in order to not fall far behind. But the borders beyond CEMAC are still closed off, with little to no chance of that changing in the near future. The approach is a managed effort, and an experimental case study for regulatory reform across a group of small, underdeveloped economies joining together.

Meanwhile, payments technology companies and MNOs alike wait with bated breath for GIMAC’s formal launch, as well as easing of extra-zone restrictions. As we have said elsewhere, technology often runs several moves ahead of central bankers’ plans. CEMAC and Cameroon are no exceptions. With a high level of mobile penetration and strong flows of regional trade, connecting CEMAC countries to their neighbors should be an obvious priority. And while GIMAC was being crafted, companies like MFS Africa have been integrating to mobile wallet systems in the region and enabling cross-border digital payments for years. In both East Africa and in the BCEAO (XOF) zone, MFS Africa has enabled cross border payments within and between regional economic zones.

“We actually connected MTN Cameroon to MTN Congo (Brazzaville) in 2017. Since then, we’ve integrated to so many other partners in the region, from banks to money transfer operators to MNOs. We are connected to mobile networks and banks in DRC and Nigeria alike - in an hour we could easily switch on these corridors. The technology is simple.”

Dare Okoudjou, Founder and CEO, MFS Africa

Regulators must balance the risk of continuing cash and other informal channels for these large cross border corridors, or adopting current digital payment channels that capture less information than traditional banks require.

It is yet to be seen what potential implications and risks may come from this petri-dish of regional interoperability bound by protectionism. The balancing act of encouraging development through integration while still guarding a domestic digital finance ecosystem, even if that domestic ecosystem is predominantly representative of foreign players, may prove challenging. And with a majority of digital finance activity originating from Cameroon, it is difficult to predict whether the benefits will be evenly distributed across CEMAC markets or concentrated in those with the most participation.

With many factors at play, like the COVID crisis and unstable oil prices, the region’s economic future is all but certain. But, if an alternative approach to digital finance integration can reap some fundamental benefits and ignite digital innovation, there is significant opportunity to be had, both for CEMAC and across Africa.

Image courtesy of Ralph Messi

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

Let Us Not Forget: The Internet Is A Human Right

We Need All Three: How ID, Finance, And Mobile Can Help The Poor