Is Gig Work Financially Sustainable?

~10 min read

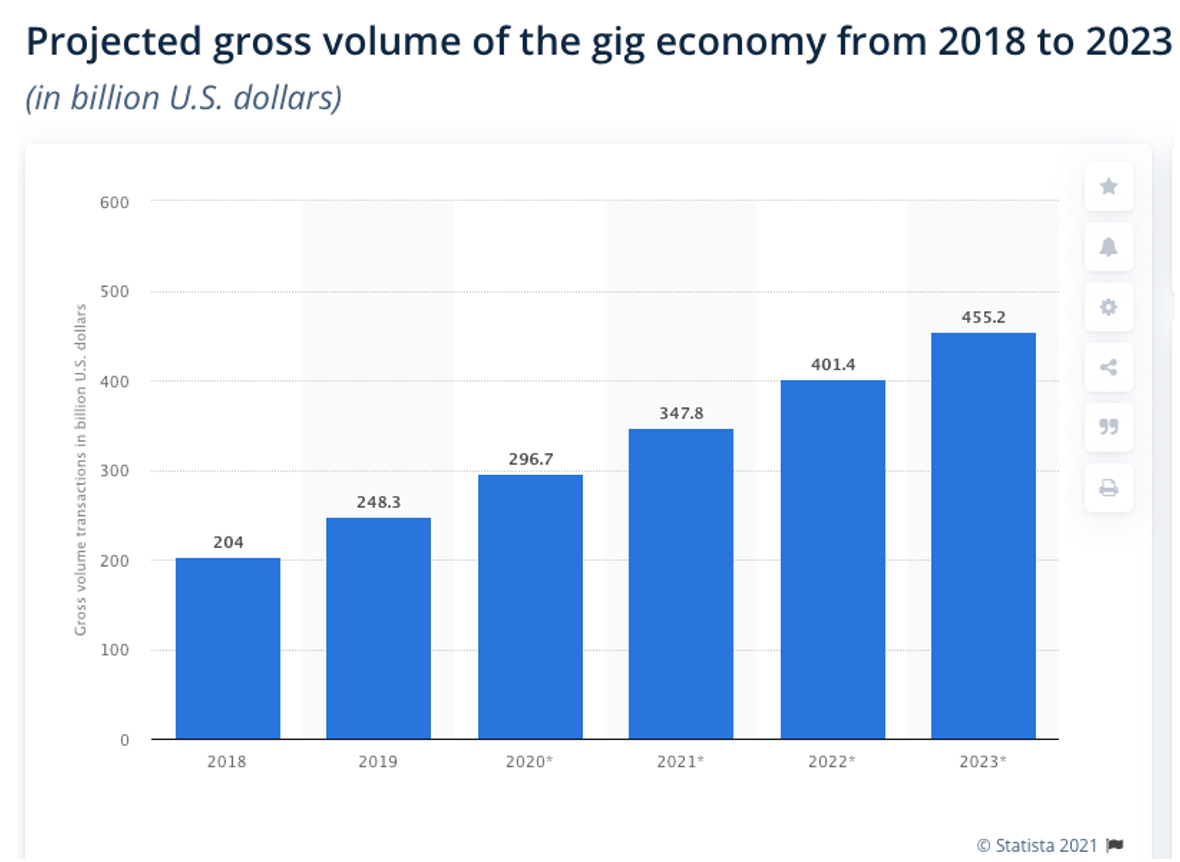

The lack of stable income from single, easily verifiable sources makes it difficult for gig workers to access traditional financial services, and the yawning inclusion gap of this sector becomes more glaring as the gig economy explodes: the sector is projected to grow to $455 billion by 2023, or more than double the sector’s size in 2018. More than a third of U.S. workers participate in the gig economy, which is also seeing explosive growth in emerging markets in places like Southeast Asia and Africa as well.

As a group that is disproportionately poorer and less educated, the lack of stable income and access to traditional financial services renders these workers vulnerable to financial shocks, as seen during the pandemic. Yet when considering how to improve the financial health of this segment through financial products, the characteristics and needs of this population are far more complex than the typical financial inclusion conversation. As markets witness a transformation of how people work, the goal for all stakeholders involved — governments, gig companies and the financial services industry — should not be to incorporate such workers in preexisting financial services ill-equipped to serve their needs. Rather, the ongoing transformation of the work sector demands an overhaul in financial approach that more holistically understands and serves these 21st century digital workers — a challenge that recent innovations are quickly making possible to solve.

The Transient Profile of a Transient Segment

In spite of the gig economy’s size and importance, we are still only beginning to learn the unique attributes of gig workers in a segmented fashion. Assessing the financial situation of gig workers in aggregate terms is a risky proposition when considering the vast differences that workers engage in the gig economy and the disparate financial situations such workers enter the gig economy in the first place. This conclusion was reached by a team of researchers from UNCDF, led by Jaspreet Singh and Audrey Misquith.

In their December report, the researchers surveyed over 15,000 gig workers from several gig platforms in Malaysia and China, measuring, among other areas, the reasons for why workers went into the gig economy, their work behaviors, the financial services they have access to and use, and several indicators relating to their financial health. Taking place largely in the first months of the COVID pandemic, the researchers were also able to measure how gig workers managed financially during the crisis.

When looking at the sample in the aggregate, UNCDF found that gig workers were generally able to meet daily commitments, but their levels of “financial freedom” — the ability to spend money on things they enjoy — were quite low, with only 13.5 percent of the Malaysia sample saying they had this financial freedom. Perhaps most alarming, only about a third of those surveyed said they would feel comfortable absorbing a financial shock of US$250.

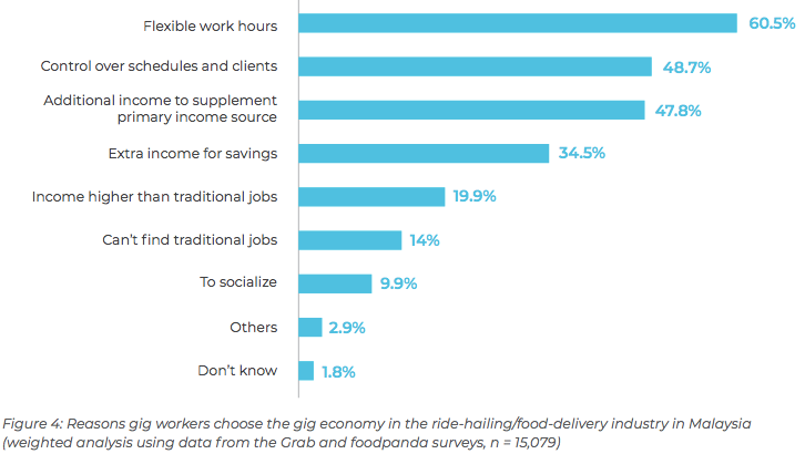

The reasons for entering the gig economy were quite varied in the UNCDF sample. 60 percent of the over 15,000 surveyed said flexible work hours was a factor, followed by almost 50 percent who said control over schedules and additional income to supplement primary income were motivating factors. Only 14 percent said that they entered the gig economy because they were unable to find a traditional job, further evidence that flexibility needed due to personal circumstances was a predominant factor in the aggregate.

Source: UNCDF

But breaking those surveyed down further by age and whether workers engaged in the gig economy part-time or full-time, the UNCDF researchers found the financial situation to be worse among workers who are between the ages of 25 and 50 and who do gig work full-time. At first glance, this may seem worrying, but it’s critical to consider from what financial situation these workers entered the gig economy. The youngest workers did gig work with specific goals in mind, like saving for a car or wedding, while older workers under 50 had higher financial commitments, and those working gig jobs full-time came from poorer and less educated backgrounds. Although gig work wasn’t sufficient for these full-time workers with families to feed to “enjoy” themselves, the income provided is typically better than the other few options available. Such kinds of findings led the UNCDF team to reorient how they viewed the gig worker segment at large.

“When we were doing our research, we kept talking about gig workers as a homogenous group, and we realized through that process that is very dangerous. There are segments within the gig worker demographic that behave very differently and that also varies very widely on financial health outcomes. It’s not just designing products and services for all these different segments but targeting them effectively so that they use those services.”

Audrey Misquith - DFS expert, UNCDF

Some of their findings surprised the gig platforms themselves. When surveying the food delivery and transportation platform Grab, UNCDF found workers in the Grab Food app were more financially healthy than those in the company’s other verticals, due to the fact that food delivery drivers were disproportionately much younger with less financial commitments. Representatives from Grab — which the researchers noted was the only platform surveyed to offer a plethora of financial solutions to their gig workers — saw this data as helpful in more effectively targeting workers with financial solutions in a segmented fashion.

The scope of financial services that surveyed gig workers used was quite limited, however — while 85 percent of those in ride-hailing or food delivery segments had savings accounts, only 43 percent had debit cards, followed by e-wallets at 28 percent, 27 percent that utilized Malaysia’s voluntary Employees Provident Fund (EPF), 25 percent with insurance, and 18 percent that accessed loans. Only 4 percent used financial planning apps.

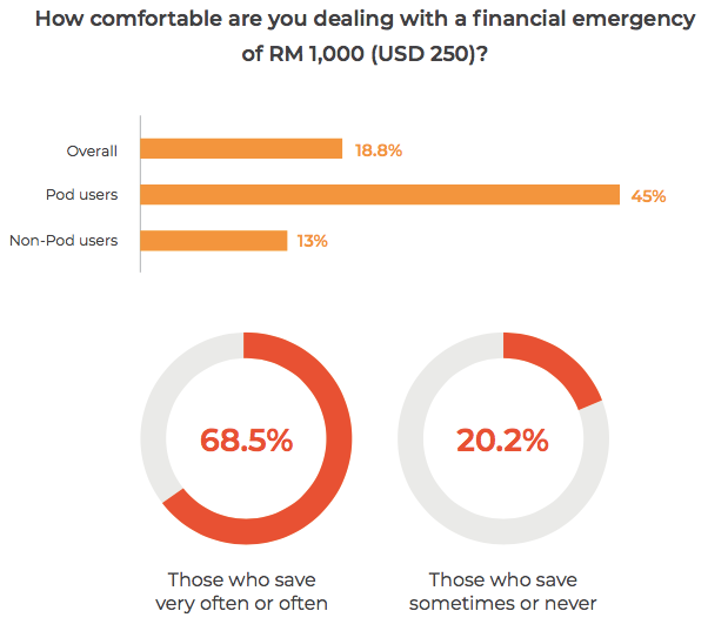

Merely a quarter of those surveyed in the rideshare and food delivery segment saved frequently, but the researchers found that regardless of income, having a pattern of saving led to far more financially resilient conditions for gig workers. In the sample surveying workers from GoGet, which is piloting a micro-savings product called Pod for its workers, users of Pod were more capable in meeting their daily commitments, and Pod users were more than three times likely to be able to handle financial shocks than non-Pod users.

Source: UNCDF

While uncertain income was the primary concern for surveyed gig workers, only a quarter of those surveyed cited the lack of social security benefits as a concern. The low levels of workers paying into Malaysia’s EPF scheme suggests both a lack of awareness as well as a resistance to paying out of their own pocket to build such reserves.

Capturing a Transient Segment

The diverse nature of gig workers is only one layer to the multifaceted issues involved in offering salient products to this segment. Gig workers often have bad credit or lack a formal credit profile, and many use multiple apps at once, making it difficult for financial service providers to accurately assess their income, which are typically unstable and varying. This uncertainty is a cause for heightened risk from the perspective of wary traditional financial institutions.

The resulting inclusion gap is being filled by fintech solutions seeking to unify gig workers’ employment history and provide tailored solutions to meet their very specific needs. A few companies are employing solutions to consolidate the scattered employment histories of gig workers. In Latin America, Belvo is solving the employment data consolidation issue through APIs and utilization of an open banking scheme to create a more unified profile of gig workers that partnering fintechs can use. In the U.S., Argyle, an employment data platform, does this backend work for fintechs as well, piping employment data over from different sources into one platform hosted by the partnering fintech.

“The key issue in the industry is that records are stored in such disparate locations in such different types of databases that it’s impossible for any business to digest that info in a scalable way without someone to do that piping work, which I think is the first layer of consolidations.”

Billy Marsden - COO and Co-Founder, Argyle

As Marsden explains, employment or work records for a gig worker are very different compared to a typical employee; for instance, a unit of work for a gig worker is often a trip with varying time and location attributes. Argyle does work with Buckle, which provides auto insurance to rideshare and delivery workers. Auto insurance for gig drivers is an essential tool in protecting themselves from unforeseen incidents, but it is very difficult for gig workers to obtain through traditional channels; auto insurance companies simply don’t have enough information to accurately assess the behaviors and risks of such customers. Argyle accesses information from several gig economy platform companies to provide Buckle with information regarding how often people are working and what days and times. By providing accurate timestamps of when gig drivers are on the job, Argyle enables Buckle to better underwrite drivers.

Among other companies it works with in the gig space, Argyle also partners with Moves Financial to provide financial products to typically excluded gig workers. An early-stage company, Moves markets itself as the only all in one financial app built exclusively for gig workers. Moves utilizes Argyle to access the gross income of workers across multiple apps to gain a firm understanding of their earnings patterns. With that information, Moves currently offers a cash advance program to gig workers as an alternative to predatory payday lenders. Many of the early-stage startups in this arena have commenced services with such cash advance offerings, owing to the lack of credit products available to the segment. Viewing this offering as a money loser to get gig workers onto their platform, Moves’ offers a cash advance of about one weeks’ worth of a gig workers’ earning, charging 3.5 percent of the value of the advance to be paid in ten weekly installments.

With gig workers currently excluded from traditional lenders and financial services, Moves hopes to build its own neobank-like platform offering an array of products specifically tailored to their needs. Moves recently announced a full-feature checking account for Moves members, shifting all income from their various gig accounts into one Moves account accessible with a Visa debit card.

According to Moves founder and CEO Matt Spoke, the maturation of B2B, banking-as-a-service infrastructure in the past couple years was a critical step in developing innovative solutions specifically designed and targeting these key demographics. Moves and likeminded companies are slowly taking business away from more established neobank firms like Chime, an offering popular with gig workers but which lacks the tailored solutions meeting gig workers’ specific needs. As it develops, Spoke envisions Moves estimating future tax liabilities and automatically deducting the necessary amounts from gig workers’ income to put into a separate account; gig workers often go into debt having not prepared for the full tax liabilities revealed come Tax Day. Spoke says Moves’ “guiding north star” is offering fractional shares of gig companies to their workers in the future — an idea that at scale can give workers unshakeable clout to impact the policies of gig companies as they have struggled to do so far.

As Spoke points out, debates in places like California over whether to classify gig workers as employees or contractors have misread the characteristics and desires of gig workers at large. The classification debate has led some of these companies to pull back on their direct financial services offerings to workers or partner with companies like Marketa, GoBank and Green Dot not to provide direct financial services, but to create sticky loyalty programs for gig workers. Uber shut down its Uber Money platform in part to shield itself from being seen as offering benefits to workers similar to an employer-employee relationship. In this sense, the public debate disincentivizes gig companies from providing sufficient financial solutions to their gig workers.

“Governments don’t understand how this market functions. What we’ve seen very clearly is that the majority — like 75-80 percent — in this market value their flexibility more than they value the sort of deemed protection that a government regulation might provide to them.”

Matt Spoke, CEO, Moves Financial

When Transience Leads to Transformation

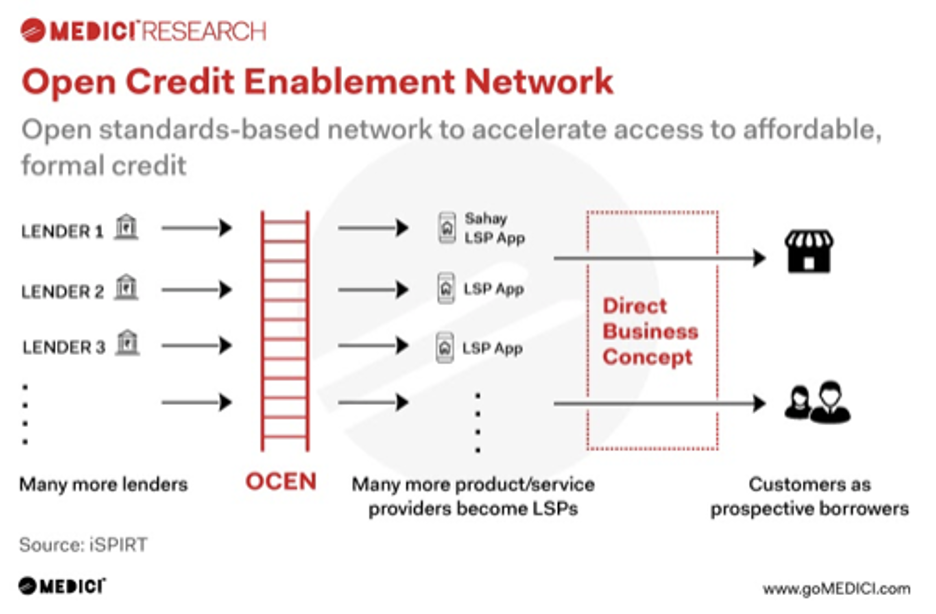

As gig companies shy away from offering robust financial service products directly to their workers and traditional financial institutions remain on the sidelines, the development of parallel ecosystems consolidating employment data to create tailored solutions gains greater importance. That isn’t to say governments have no potential role in financially enabling these gig workers. In India, authorities are able to build on their Aadhaar ID system and universal payments interface (UPI) to create consolidated gig worker profiles through more official channels. In recent months, the country has utilized its preexisting IndiaStack infrastructure to introduce its Open Credit Enablement Network (OECN), a framework of APIs for interaction between lenders, loan service providers (LSPs) and account aggregators. Account aggregators essentially perform what an Argyle does elsewhere, only through nationalized means. With such developments, India may soon preview how gig workers financially operate under more formalized and unified conditions.

But most countries don’t have the robust identity and universal payments regime that India does. In various regions of the world — with players like ImaliPay in Africa, Heru in Latin America, Moves and other players in North America and Europe — we are seeing the initial stages of these companies creating their own framework for solutions serving the gig economy. As Moves’ Spoke puts it, the end goal is not inclusion and integration with preexisting products ill-suited for the needs of the diverse gig worker class, but recognition of a transformational shift in how people earn money — and adapting products to the evolved landscape.

“Sometime in the next decade, more than 50% of American adults will end up having a primary income from freelance or gig work. That changes a lot of the basic assumptions around our financial services markets. I don’t think that the north star is can we get gig workers to access the same financial products that everyone else does. I think it’s can we build financial products that actually meet them where they are in their lives and are designed for this new characteristic.”

Matt Spoke, CEO, Moves Financial

As these products mature and specialize alongside increasingly comprehensive and granular employment data, it is fair to assume that the marginal benefits the UNCDF researchers found basic savings products had on the livelihood of gig workers will only increase as products offered and used become more sophisticated. Barring further developments from a regulatory or gig platform standpoint, the maturation of such products is critical for gig work to be not simply financially sustainable at minimal levels and in optimal conditions, but as a viable option in achieving financial freedom and resilience.

Considering the erratic nature of such work without benefits, the margin of error can be rail-thin for gig workers coming from disadvantaged backgrounds. But by understanding who a given gig worker is, why they do gig work, and what their financial and logistical needs are, the gaps inherent to such employment can be assuaged at the very least. Tailored financial products won’t altogether solve the systemic issues underlying the mass migration to gig work underway, yet they have the potential to transform how financial services address the needs of workers themselves. As gig work becomes ubiquitous, the obsolescence of legacy systems like FICO credit scores becomes increasingly apparent at scale. By transforming how we work, the gig economy can transform how we financially serve.

Image courtesy of Surface

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

COVID’s G2P Revolution: Togo as a Case Study

Emerging Market BNPL: An Opportunity for Growth and Inclusion