The Death Of Cash: Greatly Exaggerated?

~6 min read

The death of cash has been foretold for years. Among other causes, the rise of digital payment tools and proliferation of mobile devices are sometimes cited as the two main catalysts of cash’s inevitable demise. Now, a third force (this time of nature) has aligned against hard currency, in the form of COVID-19. Not only are governments explicitly restricting the use of cash (as the virus has been shown to linger on bills), but stay-at-home orders mean that digital payments, e-commerce, and online/mobile banking are, at least temporarily, replacing retail and in-person transactions. But stubborn barriers to adoption have long prevented digital payments from capturing market share -- will COVID change this calculus for good? And what will it take for societies across the world to become cashless once and for all?

Dirty Money

China and South Korea were the first countries to disinfect and isolate banknotes for the purpose of curbing COVID-19. The following month, in March, reporting in The Telegraph characterized comments from the World Health Organization as suggesting that “dirty banknotes” could be spreading the virus; WHO spokesperson Fadela Chlaib later clarified, saying the organization’s comments were “misrepresented”:

WHO did NOT say banknotes would transmit COVID-19, nor have we issued any warnings or statements about this… We were asked if we thought banknotes could transmit COVID-19 and we said you should wash your hands after handling money, especially if handling or eating food… [it’s] good hygiene practice.

Fadela Chaib, spokesperson, World Health Organization (via MarketWatch)

Officially, experts say there “isn’t much evidence” that COVID-19 can be transmitted via paper money. Coins may be riskier. However, that hasn’t stopped many officials from playing it safe. Since March, the U.S. Federal Reserve has been quarantining dollars repatriated from Asia for seven to 10 days. The dollars in question were returning stateside from COVID’s region of origin, so presumably the measures were designed to keep the virus out of the country.

In Pakistan, on the other hand, the State Bank instituted a 14-day quarantine of rupees, but in their case the currency was held under seal by the country’s various private banks. Moreover, this was not cash entering the country from abroad, but rather cash that said banks had collected from hospitals and clinics in the course of routine business. Due to the low penetration of formal banking in Pakistan (only 21% of Pakistani adults, and 7% of women, have a bank account), cash is widespread, and allowing virus-laden bills to go from a hospital to a bank branch to a customer, and then into circulation, could pose considerable risk. Additionally, Pakistan’s State Bank is encouraging the use of online and mobile banking in order to limit branch visits. This initiative, however, is hamstrung again by how few Pakistanis have formal bank accounts, as well as by the fact that only 10 million of Pakistan’s 160 million mobile subscribers have mobile wallets.

If COVID-19 is indeed cashborne (which it may not be), cash is likely not a major concern when person-to-person infection is still not entirely under control. To limit the virus’s spread, social distancing and other recommended measures are more likely to deliver results compared to locking away potentially infected banknotes.

Are you in a crowded theater? Are you in a restaurant? Are you in a Costco? You’re more likely to pick up Covid-19 from people exposure than from the type of payment.”

Dr. Marilyn Roberts, Professor, University of Washington School of Public Health (via MIT)

But cash could nevertheless be on its way out, and social distancing could be its chaperone. A consistent theme across the changes COVID has wrought is the digitization of so much of daily life -- from work, to commerce, to education, to financial services. If these changes “stick” for the months (or years) to come, it could lead cash to decline in market share as consumers and vendors alike adopt digital means of payment instead.

Stay At Home, Pay At Home

Governments on every continent have taken measures, including restricting travel, banning gatherings of specific sizes, and ordering businesses to close, to slow the spread of COVID-19. As Mondato covered last month, these measures have given rise to “digital distancing”, or the practice of using digital tools to limit personal interaction and reduce infection risk. Instead of shopping in person at a retail store, consumers are turning to e-commerce. Instead of visiting restaurants, customers are having food or groceries delivered to their homes. This pattern extends to financial services, too; since stay-at-home orders went into effect, HSBC and Lloyds Bank in the U.K. reported increases in digital check deposits of 30% and 20%, respectively.

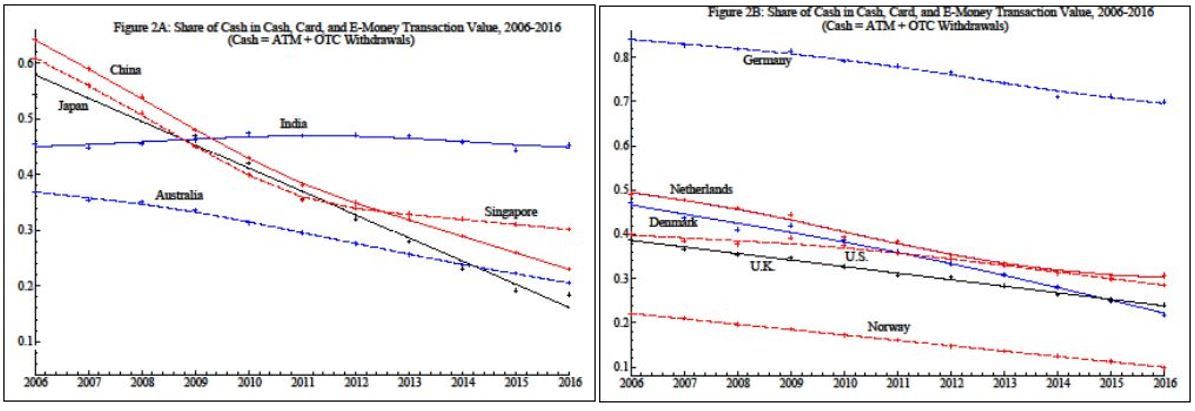

Online banking and digital payment tools have been around for years, however, and still some segments of the population, even within developed markets, prefer cash. Older individuals, in particular, are reluctant to change the way they pay. IMF researchers outlined how this trend ultimately reduces the market share of cash over the long run in a working paper:

Surveys show that younger adults favor non-cash payment methods (cards, mobile phones) over cash, while the reverse applies for older adults. Thus, natural demographic change is sufficient to explain declining cash use. As the former cohort replaces the latter one, this progression will be hard to stop or reverse.

Tanai Khiaonarong & David Humphrey, IMF

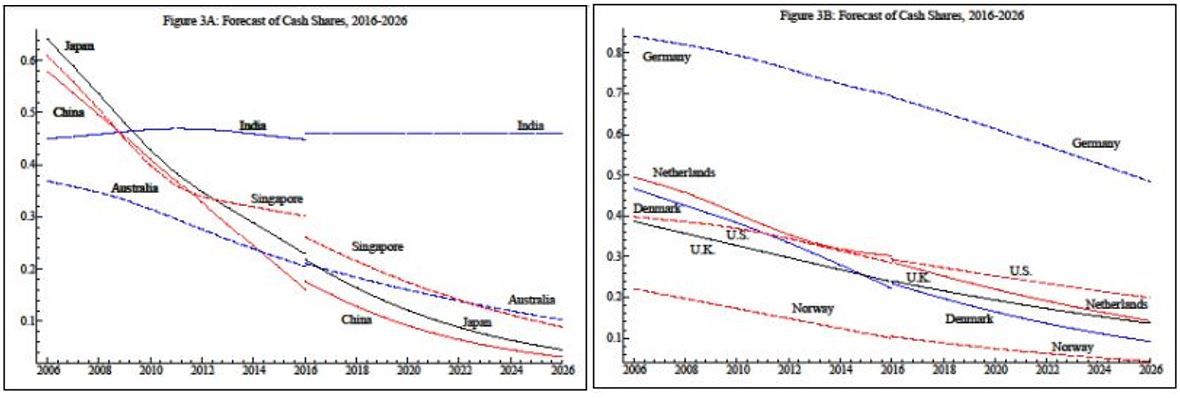

The researchers found that, all things considered, cash tended to decline in market share across the countries studied from 2006-2016, possibly driven by the aforementioned demographic phenomenon. To paraphrase: they argue that as younger, technologically savvy members of the population replace older, cash-loving ones, non-cash forms of payment will grow in market share while cash will shrink. Their forecasts for 2016-2026 reflected this trend, and saw cash decline in market share within every country studied with the exception of India.

A Silver Swan?

Enter the black swan. An event as significant as the COVID-19 outbreak has the potential to alter long-standing patterns, and in the case of cash’s declining popularity, the effect is likely to be in favor of greater adoption of digital tools. While online banking and non-cash payments are up in general due to the crisis, digital financial service providers are now successfully targeting a population segment who may have been unreachable were it not for COVID: older users.

Defined as those over 50, older users like cash, dislike digital payments, and are difficult to sway. But that is changing. This segment, perhaps more than any other, grasps the importance of social distancing as they are more vulnerable to negative health outcomes related to COVID-19 than any other group. Encouragingly, they appear to be getting the message; Paypal reported that the 50+ group was their fastest-growing segment in the U.S. in March and April as stay-at-home orders took effect. For these users, it is more a matter of safety now than of preference, and adoption across this segment could grow even more quickly as familiarity with a “gateway” platform like Paypal could spark adoption of other fintech services like P2P payments or X-pays, both of which still exhibit quite low penetration among older users.

However, if COVID is providing the spark which will fuel adoption among the 50+ crowd, the flame must be stoked and tended to by younger folks for whom digital tools are second nature. Reports of senior citizens who want to use e-wallets but don’t know how remind us that, for any society aspiring to become “cashless” or “cash-lite”, it is insufficient to simply make digital tools available; adoption must be facilitated and encouraged. While younger individuals can (and should) take it upon themselves to help older family members take advantage of today’s tech, governments can step up too. The government of Singapore, for example, operates a hub known as We Go Digital which is designed to help older Singaporeans become familiar with digital and online tools during COVID-19. The hub assures visitors that “Life Goes On… Online!” and provides basic lessons for seniors on buying, paying, learning, and even accessing entertainment online.

Life does, in fact, go on... online. Everything cash can do, digital can do better, and as populations within developed markets become accustomed to the new normal, they may find that digital tools make life easier, and will continue to use them after the dust has settled around COVID. In emerging markets, the same dynamic may take hold to a lesser extent, though the same barriers that made financial inclusion an uphill battle pre-COVID will continue to blunt the effectiveness of renewed pushes for the adoption of digital. Will cash survive this crisis? The answer is likely “yes”, but the good news is that cash is getting weaker every day, and COVID is dealing it what may prove a decisive blow.

Image courtesy of Branimir Balogovic

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

Difficult Days: How Long Can Small Lenders Last?

East Asia Reopening: A Model To Follow?