Difficult Days: How Long Can Small Lenders Last?

~10 min read

The COVID-19 pandemic is a make-or-break moment for lenders to small and micro enterprises (SMEs) and those at the bottom of the pyramid (BoP). Even before the crisis, companies in the digital lending or MFI space engaged in a high-wire act of balancing higher-risk portfolios with potentially higher profit margins, often with the help of AI-driven credit scoring algorithms, by offering loans to those excluded from traditional channels. Although these lenders vary in terms of their clientele, lending structures, and business practices, nearly all are currently facing unprecedented delinquency and default rates among borrowers. This is upending the constant growth model many of these companies rely upon to operate. In the short term, this will be bad for all lenders -- but will those who adopt a digital approach fare better?

At the same time, the crisis demands low-touch solutions to keep SMEs on financial life support and inject liquidity into businesses once the recovery ensues. After years of largely ignoring nontraditional lenders in financial policymaking, governments are incorporating fintechs and other alternative lenders in their financial relief response to an unprecedented degree. This crisis accentuates alternative lending’s greatest strengths in servicing the world’s poorest — but it also magnifies its structural weaknesses. The crisis poses the first major test on a global scale of these nascent lending industries.

The approaches taken by lenders have varied in accordance with their diverse lending structures, customer portfolios, and the region they’re operating in. But while it is still too early to know precisely what the lending industry will look like post-COVID, this high-pressure environment will be one where the cream truly rises to the top, demanding much-needed reforms in operations and customer approach as alternative credit emerges as a structural essential during this crisis.

Credit Under Pressure

Numerous other factors are in play, but the two qualities that will best predict the survival of BoP and SME lenders during the crisis will be how digitized and well-funded their operations are. In South Asia, MFI and fintech lenders have for years provided access to credit for SMEs and those at the BoP that traditional financial institutions long denied. In times of growth, with few hiccups, such lending initiatives largely worked for lenders. They could count on sufficient levels of repayments to continue funding operations or pay back their own creditors, who could be other non-banking financial companies (NBFCs) or banking institutions. The risk-reward calculus has now been fundamentally altered, however — and companies are recalibrating in different ways.

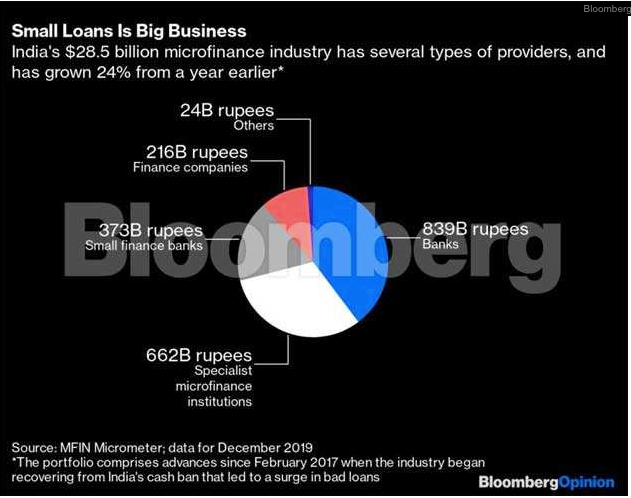

Individual MFIs fall somewhere along a spectrum of socially-driven and profit-seeking enterprises, so it shouldn’t be a surprise that as their customers go broke, different MFIs have had divergent responses. While the MFI model has proven successful and even highly profitable, its margins can be unforgiving. A slip in repayment rates from 95% to 85% would render many MFIs insolvent, as CGAP noted in March. Over two months after economies were put on lockdown, the delinquency rates have jumped way beyond that. Some firms in India have found that 90% of customers now can’t make repayments even if they wanted to, compared to 5% pre-COVID.

Lockdowns and social distancing have also greatly impeded collection efforts in South Asia, which are typically done in person by leveraging personal relationships at the village level. A forthcoming study in the Oxford Review of Economic Policy on microfinance in Pakistan during the pandemic paints a sobering picture. Surveying 1,000 microenterprise owners and about 200 microfinance loan officers, the researchers found that 70% of microfinance borrowers reported being unable to repay their loans, and loan officers anticipated a repayment rate of just 34% in April 2020 — down from 98% in February. However, while a plurality (38%) of loan officers cited non-repayment of loans as their biggest worry, 28% cited their ability to collect repayments as their biggest concern, followed by 23% who cited the challenge of staying connected with their managers or clients.

MFI’s face-to-face relationships with customers has been key in their success reaching out to poorer, rural customers, doing collections, and fostering trust. Although in many cases disbursements have been digitized, collections have generally not. The crisis may compel much-needed collection reforms on this front. According to Audrey Misquith, a digital finance expert at UNCDF and a former credit manager at State Bank of India, collection practices among banks and MFIs in India can be aggressive, in which credit officers come to villages to intimidate delinquent borrowers through social shaming. In her experience, such tactics fared worse compared to when they worked with borrowers to restructure loan terms. With loan officers unable to collect debts in person, MFIs must digitize if they’re to survive — and with such high levels of delinquent borrowers, the best option for creditors might be to work through digital channels to restructure loan terms with customers — or otherwise not get anything back at all. Depending on an MFI’s approach during the crisis, hard-earned trust between MFIs and clients can be solidified or wiped away in an instant.

Fintech lenders were far better positioned in digitizing collections than MFIs in South Asia before the crisis. But many of these non-deposit accepting fintech lenders —grappling with swells of non-performing loans — are faced with the challenge of paying their own creditors. Some creditors are proving more forgiving than others.

Where the pressure points fall in the SME lending ecosystem is largely dictated by the emergency regulatory regime the lending ecosystem is operating in. Many governments in South Asia and the rest of the world have extended loan moratoriums, in which borrowers are relieved from at least some of their repayment duties during the crisis. But such moratoriums don’t completely remove fiscal pressures; in many cases, they’re simply putting them off until a few months from now when lockdowns may have eased, but the financial crisis has not. Without restructuring loans, a borrower’s monthly loan obligations might be greater than before the crisis at a time they are trying to recover — setting up for a potential avalanche of defaults once the moratoriums end. Moody’s warned in April of the buildup of credit that may occur in countries in the Asia Pacific offering loan moratoriums, like China, Australia, Malaysia, and India.

Most government moratorium initiatives promise to subsidize some of the cost for lenders, and countries like Saudi Arabia may have the coffers to offer more sufficient relief. But the implementation of such subsidies in a subcontinent of some 2 billion people does not necessarily correspond with promising newspaper headlines.

“Governments are saying we’ll subsidize financial institutions or MFIs, but MFIs and banks know especially in the South Asia context that this takes a while to actually happen. They will just kind of follow what government says, but we are not seeing that materialize. We are seeing that clients are still being required to pay, and if they haven’t paid, they’re showing up as defaulters on the banks or the MFI system.”

Audrey Misquith, UNCDF

As Misquith notes, this is not the case across the board; social-minded enterprises are employing creative solutions like crowdfunding to help borrowers, and some well-capitalized lenders are allowing borrowers to forego the interest or principle payments on their loans. But the Pakistan study also revealed a gap between rhetoric and action. Although 60% of loan officers said they offered repayment flexibility to borrowers, 96% of clients said they had not been offered repayment flexibility during the crisis.

Lenders are confronting a tightening liquidity crunch. Amidst such uncertainty and fiscal strain, many alternative lenders have drastically cut back on loan originations, declining to lend to businesses most affected by the crisis. Some microborrowers like food vendors — small enough to close up shop without accruing much fixed costs — have simply stopped taking out loans, but other SMEs have obligations they must meet. Though lenders are acting fiscally responsible in the short term, shrinking loan portfolios can leave SMEs in most need without a life raft — barring government intervention that adequately reaches SMEs. This may bring the portfolios of some alternative lenders closer in line to traditional lenders — less risk, but more exclusive.

A willingness to offer credit to higher risk segments is essential during the crisis, however — and even the Indian government has started to recognize that. India’s fiscal policies have traditionally been dictated by the big banks, glossing over the needs of nonbanking financial companies. But just recently, the government of India announced it would provide some liquidity relief to non-bank lenders. While there is some skepticism that this will actually reach the NBFCs most in dire straits, in symbolic terms, this signifies long-due recognition of the structural importance these NBFCs possess in servicing India’s SMEs.

The robustness of liquidity and moratorium assistance programs will greatly influence what shape countries’ lending ecosystems will be in post-COVD 19, and other digital-friendly reforms might help lenders stay afloat . Allowing eKYC among NBFCs in India might help keep rural borrowing stable ; CreditInfo linked stable lending volumes in countries during the crisis to more lax eKYC laws, in comparison to countries demanding wet signatures that have seen a noticeable drop.

But at the end of the day, institutional support will be everything, whether that be from the government or financial backers. Fintech lenders like the Capital G-backed Aye Finance may be able to weather rising defaults and a slumping portfolio and even create more favorable terms for distressed borrowers— but that isn’t the case for the many start-ups who are laying off workers or shutting down completely as cash dries up.

Meanwhile, In East Africa

In Sub-Saharan African countries like Kenya, similar dynamics are playing out in the primarily mobile-driven credit platforms. Mondato has previously framed the largely unregulated landscapes that digital lenders operate in through the lens of Sub-Saharan Africa, warning in another post on financial health that with high interest rates leading to worrying default rates in Kenya, fintech lenders may not be prepared for a downturn in the economy.

While the Kenyan government has implemented some reforms in the past year, that downturn has now come without warning, and judgment day is upon these fintech lenders. Digital loans defaults rose to 23% in April, leading non-bank mobile phone lenders to significantly reduce their credit or go out of business altogether.

The situation among mobile phone lenders is a bit different considering many of them — about 70%, according to Sakshi Chadha of GSMA — partner with banks or other providers who likely take care of the balance sheet. But without proper intervention, the entire ecosystem is at risk. Kevin Mutiso, a spokesperson for Kenya’s Digital Lenders Association (DLA), said in an April 30 interview that “without financial solutions cascading down to our customers,” two thirds of digital lenders will go out of business. Mutiso expressed hope of working with banks and the government for a guarantee scheme, pointing to a think tank calculation of 100 billion shillings (or a bit less than $1 billion USD) needed to both keep SMEs alive and to offer working capital to restart businesses. The Central Bank of Kenya recently greenlighted such an initiative, but the terms and mechanisms remain unclear. The Kenyan market is already oversaturated with lending apps, many of which are criticized for predatory interest rates, so if the result is consolidation and not collapse, the industry might come out of the crisis in some ways healthier than it had been before. To help keep clients afloat, some digital lenders are enacting changes like reducing maximum loan amounts, extending repayment periods, and slowing down loan increases for repeat borrowers. Such policy changes might be best for lenders, too, if the alternative is massive client defaults.

Similar to India, Kenya’s regime had historically left digital lenders alone, in this case operating in a proverbial Wild West of lax regulations. But here, too, the regime has shifted greater attention to the lending sectors that SMEs are using. KCB Bank, one of Kenya’s biggest banks, is lending $284 million to businesses and individuals through mPesa. Predatory loans led to more than 2.5 million Kenyans being negatively listed with the credit reference bureau (CRB) before the crisis, making banks and SACCOs reluctant to offer them loans. In response, the Kenyan government announced a fine of 2 million shillings for every defaulter that banks, SACCOs, and MFIs deny loans to because of a negative credit rating, in hopes of cleaning up the CRB blacklist. Though well-intended, this heavy hand might also force lenders to take on more risk than they can handle. Therein lies the catch-22 of keeping business going with insufficient business coming in: regulatory regimes and lenders alike must strike a balance between providing much-needed credit to distressed sectors and maintaining sustainable balance sheets.

New Responsibility, New Risk

A common thread of governmental fiscal reactions to COVID-19 around the world is the unprecedented turn to alternative lenders, whether it be MFIs, fintechs, or other nonbanking financial companies. The U.S.’ PPP loan programs for small businesses was originally open only to depository institutions, but within a couple of weeks, the U.S.’ Small Business Administration began opening it up to other lenders as well. Australia has also opened up its lending guarantee schemes to nonbank lenders. This incorporation of nonbank lenders has understandably led to worries of lightly regulated fintech loans running amok, but it solidifies alternative lenders’ standing as a systemic conduit for SME financing.

“There’s an increased awareness that small and medium-sized enterprises are reliant on new forms of credit from new types of institutions. These programs have evolved and are evolving to account for that development. The old way of having support programs just run through traditional banks isn’t going to work because that’s no longer where people are exclusively getting access to credit."

Christian McNamara, Yale Program on Financial Stability

McNamara’s team at Yale has dug into the nature of government bailout measures for small businesses around the world during the crisis. At the heart of governments’ unenviable task is figuring out how the burden — and risk — is properly distributed among borrowers, lenders, creditors, and treasures. Countries as varied as Germany and Colombia have increased their loan guarantees and affixed interest rate ceilings that are low for distressed borrowers but not too low to disincentivize participation among lenders.

In both the micro and macro, fiscal pressure points won’t subside, but be redistributed. Lenders must weigh how much relief they can provide to borrowers against their own balance sheets, and their creditors or investors must determine this balance as well. The levers of incentives and controls that monetary regimes employ will impact these dynamics on a global scale. But aside from the extent and depth of the crisis itself, it will be the fiscal preparedness, digitization, and operational nimbleness of alternative lenders that will most determine how viable they remain, let alone how effective they are in emergency fiscal relief efforts. As a young industry experiencing growing pains leading up to the crisis, alternative lending must now grow up — and fast.

Image courtesy of Aniruddha Bhattacharya

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

Remittances: Still Strong, Still Evolving

The Death Of Cash: Greatly Exaggerated?