Inclusive Insurance: Bought, Not Sold

~6 min read

In his foreword, Denis Duverne, Chairman of the Board of Directors at AXA, poked fun at the insurance industry, besmirched as it was by products that are "sold not bought." His comments were part of a larger report, a collaboration between the Institute of International Finance (IIF) and the Center for Financial Inclusion musing on the state of insurance for customers at the base of the economic pyramid. But as the name inclusive insurance connotes, the expectation this time is higher - there should be value, and that value should be sustainable - given especially the income brackets involved. Insurers are nestling into this new customer segment through budding technology, business models and product designs.

Bells And Whistles

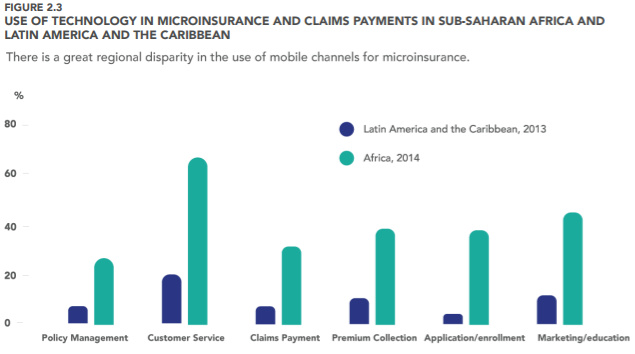

The mobile remains the uniting component of much innovation that touches the microinsurance sector. This isn't a particularly ground-breaking concept; Mondato has previously detailed some of the variations of mobile-money enabled insurance, especially as it pertains to the activities of Mobile Network Operators. But, the mobile, as far as mobile insurance goes, has brought more to the the table than just frictionless premium payments, streamlined claim submissions or customer stickiness. The benefits of the mobile are spilling over into other sections of the process, like customer service, education, enrollment and policy management.

Source: Inclusive Insurance: Closing the Protection Gap for Emerging Customers

Source: Inclusive Insurance: Closing the Protection Gap for Emerging Customers

The mobile, too, remains a powerful agent of growth for players other than telcos, as has been demonstrated by Banco Davivienda, the second largest bank in Colombia. Shortly after cinching its contract with the government to disburse conditional cash transfers (in other words, digitizing the Más Familias en Acción program) through its mobile wallet DaviPlata, Banco Davivienda quickly secured a mobile money market leader position.

The mobile again resurfaced as a device of catalytic consequence when Banco Davivienda ventured into the world of commercialized inclusive insurance. The bank's life insurance product will, in exchange for an annual premium of $10 USD, guarantee $1,000 USD to the direct relatives of the holder in addition to up to $700 USD in funeral coverage. Its roll-out is capacitated by DaviPlata, thereby creating a paper-free enrollment that has already converted 10,000 customers.

So while the medium that most obviously delivers innovation in microinsurance is still the mobile, bells and whistles are sprucing up the foundations. Digital identifications, many of which store biometric details, are rendering on-boarding a virtual process. Artificial intelligence is imparting to providers a more granular view of customers' profiles, which then informs pricing structures. Zhong An, the first online-only insurer in China, projects rates of returns and warranty claims with the help of artificial intelligence for online retailers, who then capitalize on this information to determine profitable price points.

Internet of Things, too, is not only better equipping insurers to understand the complexities of risk (like the relationship between historical satellite data and agricultural yields), but minimize it. As of mid-2017, Lumkani had installed a network of nearly 7,000 fire-detectors in Khayelitsha, a South African township, which is managed by one central smart device that zeros in on the blaze's exact GPS location through SMS communication and then notifies the proper emergency services. Nearly 10 urban-infernos have been averted since Lumkani introduced the doodads in 2014.

The Insurer That Pays Claims

Conventional wisdom has taught the average consumer to distrust the motivations of insurers in regard to two things: premiums and claims. The at-odds incentives were made clear in the aftermath of Hurricane Harvey in the United States, when insurance companies - who are legally responsible for losses caused by wind but not flooding - were caught red-handed tampering with original damage reports. Fabricated expert testimonials and evidence charged flooding as the primary culprit thereby ceding the insurers' financial accountability.

But, if inclusive insurance is to be bought not sold, the value proposition underpinning it must be honored. Pioneer Insurance in the Philippines recognized microinsurance customers' dissatisfaction with claim filing, and vowed to improve it. It set out to reduce the turnaround time between a claims submission and payment to five days across all product lines. Then, the microinsurance unit, which is governed by its own underwriting and settlement authority for flexibility's sake, overhauled its operations to relieve pain points for low-income users.

Accommodations were put in place for special circumstances. One such case is the unending loop that often plagues death policy beneficiaries. Hospitals do not release a death certificate (a requisite to initiative the claim process) until medical bills are squared away. However, insurers will often refuse to foot the bill without the certificate, resulting in a frustrating spiral for clients who do not have the upfront cash. Pioneer amended this guideline, and now sends representatives to the hospital to verify claims independent of the certificate.

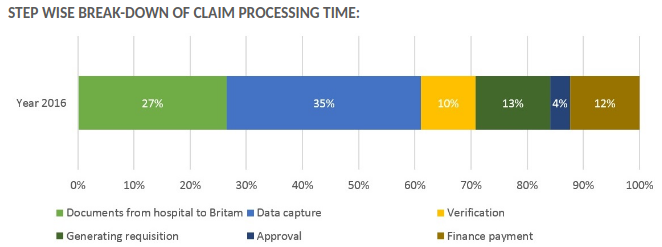

Streamlining the procedure around claims is a priority for all inclusive insurers, as it solidifies trust with its base. Britam’s Microinsurance in Kenya investigated its own bottle-necks in relation to its medical insurance.

Source: Getting To The Bottom Of Claims Turnaround Time

Source: Getting To The Bottom Of Claims Turnaround Time

Digitization (likely through the mobile) can shorten waiting times of many of the steps, from document transfer to finance payment. This, in addition to other more fringe technologies, like relying on drones to access isolated or hazardous areas after disasters to collect aerial data and gauge loss through imagery analytics, is optimizing the mechanism most fundamental to the buyers of inclusive insurance in realizing its value.

Appetite For Risk And Reward

Increasingly, insurers and distribution partners are envisioning microinsurance as a driver of revenue growth (evolving from freemium-type business models), as the size of the middle class in emerging markets billows. Each, however, is still hard-pressed to strike out individually, as insurers bring the assets while distributors offer the means to scale at low-cost margins. And although the relationship between the two remains mutually beneficial, that is not to say it hasn't undergone change.

"Once you have used free insurance as a way to entice consumers into the insurance ecosystem, there is an opportunity for expansion. In mature markets, like Ghana, our call center is phenomenally productive, with 82 percent purchasing an insurance product after an informative three minute call. While we call on behalf of the partner organization, whether the telco, bank or otherwise, we assume the financial cost associated with those sales, which is considerably different to our original models that gravitated away from risk. In fact, sometimes now we even subsidize free insurance products in exchange for long term access to mine our partners' databases."Richard Leftley, Chief Executive Officer of MicroEnsure

The profitability of microinsurance is no longer an untested concept. Allianz SE, invigorated by the early success of its credit life product in Indonesia, expanded its trials in microinsurance into a full-fledged Emerging Consumers division. By way of over 700 distribution partners across across 11 markets, the division has achieved similar margins to Allianz's more conventional products, earning more than $357 USD million in premiums from 55 million people.

Diversifying Business Lines

The AIDS epidemic of the 1980s and 1990s overwhelmed Africans, with 40 percent of the continent's inhabitants anticipating a family death within a year. It is in the context of this anguish that woke insurers up to the demand for life microinsurance ranging from credit life and funeral coverage to savings and pension products. This developing insurance penetration, coupled with a real possibility for revenue generation, have pushed both insurers and partners out of their comfort zone.

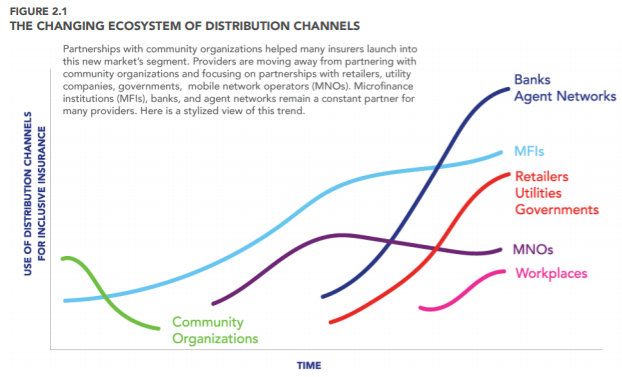

Source: Inclusive Insurance: Closing the Protection Gap for Emerging Customers

Source: Inclusive Insurance: Closing the Protection Gap for Emerging Customers

With a more variant buffet of distribution channels up for grabs, innovative approaches to inclusive insurance are forming. The most avant-garde of these is perhaps insurance blunting the toll of climate change. The African and Asian Resilience in Disaster Insurance Scheme (ARDIS) - directed by VisionFund International and Global Parametrics - will hedge the full-impact of droughts in Kenya, Malawi, Mali, Zambia and Cambodia, and tropical cyclones in Myanmar on women farmers. And while this is just the tip of the iceberg (albeit perhaps an ever disappearing iceberg), inclusive insurance is reacting to its clients' tangible needs, a promising start to being bought, not sold.

Image courtesy of Asian Development Bank

Click here to subscribe and receive a weekly Mondato Insight direct to your inbox.

Chilly Winds Of Change For Banks?

Zimbabwe's Cash Crunch: Boom Time for MNOs