Can the ABC Model Power Digital Finance?

~9 min read

Against the backdrop of a widening ecosystem of energy supply technologies and business models, digital finance is seen as both a beneficiary and a key enabler of financial inclusion. But mobile network operators — the heavyweights of infrastructure in emerging markets by a long shot — have historically been reticent to exploit the obvious synergies between the business of energy provision and that of digital services. This week’s Insight illuminates some of the touchpoints between power, digital connectivity, and financial inclusion to ask: what will it take to break down the silos separating the businesses of electricity and digital finance?

The Power of Digital

Despite notable progress over the past decades in widening access to electricity, the COVID-19 pandemic has threatened to derail the momentum of the UN’s Sustainable Development Goal (SDG) #7: “access to affordable, reliable and modern energy services.” Analysis from the International Energy Agency (IEA) suggests that the onset of the pandemic caused a 4% increase in the number of Africans without access to electricity — the first time electricity access rates have dropped relative to population growth since 2013. Increasing recognition of energy as the ‘golden thread’ weaving together the 17 SDGs, along with the Russia-Ukraine natural gas crisis, has put energy security back at the center of both business and political discussions around the world.

In no-grid and bad-grid environments in Africa and much of the world’s emerging markets, however, the critical relationship between energy and uptake of digital connectivity is nothing new. The meteoric rise of commercially-funded solar lighting products was notably enabled by Pay As You Go mobile money technology paired with remote locking, which nudged remote and rural users towards using mobile money systems as a mechanism for converting a high CAPEX obstacle for purchasing micro-utility assets into a streamlined energy-as-a-service play, as Mondato previously discussed.

Meanwhile, momentum for mini-grids has continued to swell since 2019, with increasingly sophisticated modeling systems converging around the importance of independent generation and distribution networks for communities beyond immediate proximity to legacy grid infrastructure.

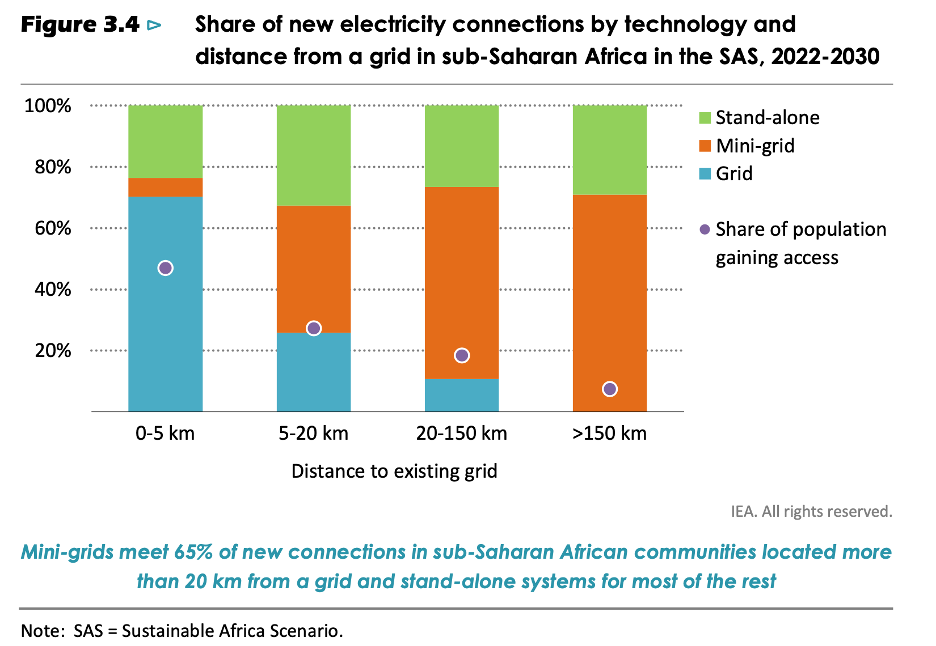

Source: IEA Africa Energy Outlook 2022

Whatever the supply modality of electrons, however, the synergy between electricity, digital connectivity and the ecosystem built on top of it seems clear. As GSMA research on the consumer impacts of PAYGO solar home system users notes, “by far the greatest impact on increased data and voice usage is that [solar home systems] allow users to charge their phones more easily and, therefore, use their phones more often.”

GSMA (2020) The Value of Pay-as-you-go Solar for Mobile Operators

Indeed, particularly for the poorest, powering phones is the primary use case for electricity; one could thus say voice calls, texts and apps collectively represent the most important demand for the flow of electrons as an ‘intermediate input’ for the financially excluded. After all, mobile phone ownership is by far the most ubiquitous (and often, the only) electronic appliance owned by the world’s bankless — with a monumentally important transition towards smartphones unfolding this decade, as Mondato has previously described. So why don’t telecom and digital finance operators get into the business of energy provision, or vice-versa?

The ABCs of Power & Finance

The notion of combining the operations of mobile coverage with those of electricity provision is not new. In fact, the concept of using telecom towers as a base station for power generation and distribution to nearby communities has been conceptually described in energy access literature for decades under the catchy moniker of the “anchor-business-community” (ABC) model.

In the simplest formulation of the ABC model, the energy supply of the largest demand center in a given community should be significantly oversized relative to its need. Excess generation is then marketed firstly to local businesses, then to local households who would otherwise be economically unattractive to supply.

The ABC model is conceptually attractive, but it’s difficult to implement in reality, given the radically different techno-economics of supplying different business use-cases; a factory using heavy duty motors may need a power supply able to tolerate significant voltage and frequency swings off of the standard 220 volts and 50 hertz, while sensitive long-range communications equipment like those on telco towers may require the exact opposite. Reliability standards for towers aim for the “4-9s” — 99.99% uptime — while newly connected remote households, for their part, may not even have the cash or the machines for more than a few dollars’ worth of kilowatt-hours per month, much less 24/7 power, undermining the whole economic rationale of oversizing for universal access.

As it turns out, electricity is not as standard a commodity as it may seem on the face of it, and particularly in smaller, remote communities, satisfying everyone at once is no easy feat. As a result, the complexities of which party might finance, own, maintain and bill for which infrastructure services across the radically different electrical needs of households, small businesses, factories or telecom towers has to date seen limited growth outside of India, where companies like Husk Power Systems and OMC Power have specialized in the model.

Yet given the relative omnipresence of telecom infrastructure in emerging markets — particularly compared to other forms of infrastructure like electricity grids, water distribution networks or banks — the potential for towers in particular to boost power supply economics remains enormous.

Of Towers and TESCOs

Part of the reason why the telecom-power gap has yawned intractably wide is that mobile network operators (MNOs) have been too focused on simply figuring out how to most efficiently manage their own fleets of radio and transmission assets like towers, transmitters and receivers; indeed, it was only in the late 2000s that specialized telecom tower companies (TowerCos) emerged to at least take the burden of building and maintaining towers in remote locations off of MNOs’ plates, allowing them to focus more on customer experience and sales. TowerCos, in turn, started to outsource their energy supply requirements to energy specialists less than a decade ago, according to a 2021 IFC report, as TESCOs: Telecom Energy Services Companies.

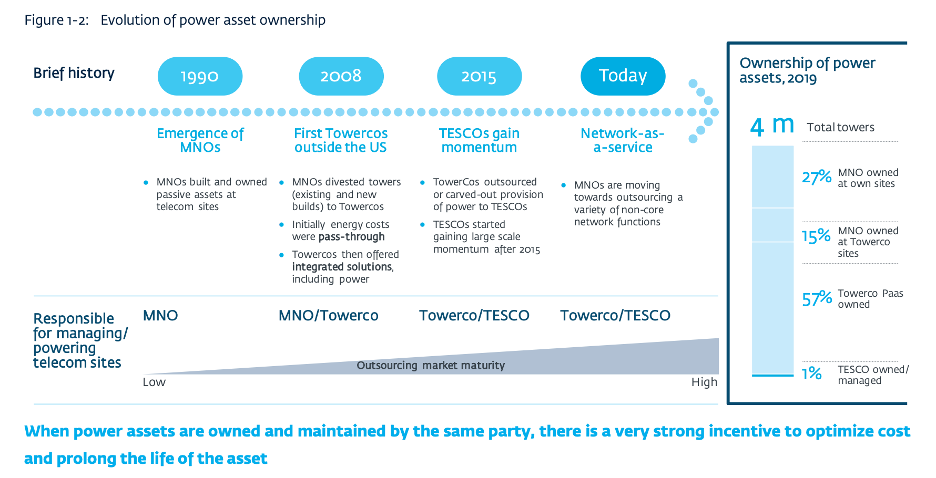

Source: IFC

Today, the burgeoning TESCO landscape of players principally serve TowerCos, but the IFC report predicts demand to increasingly come directly from MNOs, as TowerCos seek to learn from the energy specialists they have until now outsourced to. This trend back towards vertical integration of energy management of data transmission infrastructure could be a good thing for breaking down the energy/DFC silo. In MNOs’ drive towards operational efficiency through outsourcing tower operations, one element that’s gotten lost in the cracks is the incentive for maximizing energy efficiency, decarbonization and, most importantly, exploring synergistic power-digital connectivity business models.

Digitizing Utilities

As Mondato has previously covered, the interface between utility services like water, electricity and sanitation has in the past several years converged with the digital finance and communications ecosystem in a big way. In fact, the origin of GSMA’s Digital Utilities program emerged, in its earliest days, from interest in the ‘minigrid for mobile’ version of the ABC model. George Kibala Bauer, Director of GSMA’s Digital Utilties program, highlights some of challenges that have impeded widespread scaling of the model as well as some of its successes since the program’s inception:

“In the early stages of our Digital Utilities work around six or seven years ago, we were observing a huge mismatch between the needs from the telecom perspective, which thought about the ‘anchor-based-client model’ at a large scale — hundreds of towers at a time — and that of minigrid providers, on the other hand, which could only deliver on a one- or two-tower pilot. This has changed significantly, both on the solar and telco side. Both are far more mature, capable of deploying more rapidly and at a much greater scale.”

George Kibala Bauer, Director, Digital Utilities, GSMA

Bauer notes that despite several strong success stories even beyond Husk and OMC — like GhamPower in Nepal and Electricité de Madagascar — the familiar minigrid scaleability challenge persists as a consistent impediment to growth:

“Fundamentally, there haven’t been a lot of blueprints to scale. Each one that has successfully grown has been quite unique in its partnerships and agreements, which makes it difficult to replicate. In particular, that’s the minigrid sector in general — there is a uniqueness to each market, in population size and density, in regulation, and in the wider enabling environment. But there are also factors unique to the ABC model in particular such as geography, incentives and ownership dynamics.”

George Kibala Bauer, Director, Digital Utilities, GSMA

Bauer noted, however, that advances in data-driven planning, project preparation, finance and regulation ais making the model more viable, particularly in markets with weak central grid coverage, like Nigeria, where GSMA's model predicts over 26,000 off-grid and bad-grid towers to be located.

Kyle Hamilton, Senior Manager of Strategy and Partnerships at Nuru, an energy supply company in eastern Democratic Republic of the Congo, noted how essential powering these towers is to not only their business but enabling a wider array of digitally powered use cases.

“Powering towers is critical to our business model in general: they tend to be really reliable customers, both with respect to predictable demand loads as well as payments. So we’re always looking to work with MNOs to assess their energy needs and co-create plans together.”

Kyle Hamilton, Senior Manager of Strategy and Partnerships, Nuru SARL

In this fast-growing, million-strong city bordering Rwanda and Lake Kivu, telecom towers abound, both those managed by prominent TowerCos like Helios as well as the major MNOs: Vodacom, Orange and Airtel. Nuru’s innovative solar grid powers no less than six of the towers in Ndosho. Here the overlap between energy supplier and telecom infrastructure is made concrete: despite still being a relatively small company, Nuru is in constant communication with the different telecom players, sharing data and expansion plans so as to identify possible co-locations for new parts of the growing city, or underserved cities in the vast eastern territory. These kinds of conversations are critical for bridging the gap between power and the telecom layer — serving to crack open the door wider for deeper collaboration along the digital finance stack.

“With regards to operations and hardware like smartmeters, mobile money is a key piece for us. Anytime you can reduce friction with customer engagement and service, that’s always a plus. Having mobile money payment as a default should reduce customer time, keep things cashless for us as a company, plus it gets people used to using financial tools that make them more attractive customers for us.”

Kyle Hamilton, Senior Manager of Strategy and Partnerships, Nuru SARL

For energy service providers like Nuru, the opportunity to grow with the dynamic telecom industry thus represents multiple opportunities — not only to ‘go Dutch’ on the infrastructural expenditures required for economically addressing underserved markets, but also to expand the relationship into other services at the intersection of power and digital payments: mobile money API integrations for customer bill-pay, automating salary disbursement and pay for maintenance jobs, or even bundling “power+services” like appliance financing or satellite TV subscriptions.

Step 1: Power Them Towers?

Once energy suppliers prove their salt in the tower supply market, the market segment should sit front and center in long term expansion strategies; the IFC estimates that power generation costs could account for as much as half of total site costs in bad-grid and off-grid sites, which are projected to grow by 22% over the next decade, principally in Sub-Saharan Africa and South Asia. Partly driven by the telecom industry’s commitment to go carbon free as well as the increasingly competitive nature of distributed renewables versus OPEX fuel, TESCO sites are expected to quadruple in the same time frame.

This is perhaps the thinking behind recently announced partnerships between BBOXX and Orange in the DRC, a collaboration which aims to take a crack at the ABC model in both rural and urban contexts. Indeed, the French telecom giant has taken a front-row position among major MNOs in investing in innovative business models to complement its airtime and data bread and butter, from accelerating low-cost technologies to expand wireless coverage, to developing utility-bill pay smart-meters. The collapse between digital finance use cases and power supply is clearly shrinking at the margins; the question is who will manage to boldly straddle it.

As energy supply technologies and models emerge from their startup growth pangs, a critical signal of their maturity to this end will be in their ability to crack the code in working with MNOs. The first step would be to demonstrate their ability to support and supply power to tower fleets at a scale noticeable by these unrivaled behemoths of emerging market infrastructure. It is not clear that this is an absolute prerequisite for the next step of the power-digital synergy, which would look like a concerted effort by the energy-telecom partners to promote both energy services and digital finance uptake simultaneously. But given the multiplying pressures globally to rethink energy supply, security, efficiency and decarbonization — it may be the most obvious place to start.

Image courtesy of Gabriel Castles

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

Brazil’s Pix: Should Instant Payment Rails Be A Public Good?

Impact Investment: Is Standardization Possible — Or Desirable?