Digital Finance Is As Important As Ever During COVID-19

~9 min read

History tells us that The Black Death was a catalyst in shifting Europe’s economy away from the feudal system of the Middle Ages towards the early stages of the modern capitalist economy. About half of Europe’s population died then, depriving landowners of their vast peasant workforce. Wages for suddenly in-demand peasants rose, and landowners shifted from labor-intensive grain farming to animal husbandry, increasing productivity and changing what Europeans ate. Those who suffered likely didn’t focus on matters like a slowdown in early global trade, collapsing supply chains, and skyrocketing prices. To make matters worse, increases in nominal peasant wages were offset by rampant inflation. And yet, from the detached perspective of history, critical economic advancements emerged.

More recently, the 2003-2004 SARS outbreak decimated the Chinese economy, but it gave birth to Chinese e-commerce as we know it. JD.com went from a chain of small electronics shops to an e-commerce superstar serving those shuttered away during the outbreak. Alibaba became the source for foreign businessmen to receive Chinese products. Taobao launched in July 2003 during the middle of the outbreak and, aided by culturalization efforts, soon surpassed eBay as the top P2P marketplace in China.

With the world now gripped by a novel coronavirus pandemic forcing citizens into their homes, it is dawning on people that their lives won't be the same in the coming months. Stocks markets have tanked, lockdowns and quarantines have halted commercial activity, and rounds of layoffs and business closures are only just beginning. But inevitably, crisis compels innovation. Our global economy will not look the same when the pandemic subsides — especially when it comes to financial services and everyday transactions. The shape and extent of this economic transformation will vary, but the engine for a transformation in financial services and beyond will, in all likelihood, be digital.

The Original Host & The Strongest Immune System

It is apparent by now that measures like social distancing are affecting consumer habits. In spite of disruptions to the supply chain — which may worsen as the crisis deepens — e-commerce businesses like Amazon Prime have seen online shopping surge and telecommuting gain acceptance as people are forced to remain at home. Albeit by necessity, people are altering their routines to mitigate human contact. These changes are far from seamless, and digital operations are unlikely to expand their capacity sufficiently to meet spiking demand, as some fear and early evidence supports. In the immediate sense, such dramatic shifts in economic activity are a tremendous net negative — but digital financial solutions may be the best alternative in the interim.

China was the first country to confront the challenge of COVID-19. When the nation enacted the largest lockdown in human history of 46 million people total, shuttering businesses and all public life, it jeopardized the Chinese economy. But China was uniquely equipped to adapt to such circumstances. As the world’s leader in digital payment usage thanks to titans like Alipay and WeChat Pay — and their superior self-sustaining digital ecosystems— consumers there simply leaned more heavily into the formidable digital financial tools at their disposal, with e-commerce giant JD.com reporting a 30% rise in the volume of goods delivered during the outbreak.

But it isn’t merely that China has seen wider adoption of digital financial products during the crisis. Even more critically, the nation has seen an accelerated, ongoing transformation in commerce generally. It began when delivery app Meituan Dianping launched a “contactless delivery” initiative across China. Then, Alipay opened its platform up to third parties to create programs designed to help consumers on lockdown cope; within a week, developers had created 181 mini programs designed to enable “contactless” delivery services across China in areas like grocery deliveries and legal services. One mini program providing free medical consultations by AliHealth received 700,000 visits daily. JD and SF Express went on to introduce driverless delivery cars and drones, respectively, to deliver medical supplies to quarantined hospitals. Driverless delivery vans and robots were then employed to aid quarantined populations with food and supplies, with local authorities offering to subsidize up to 60% of the cost for driverless delivery vans being rolled out by start-up Neolix. When China built Huoshenshan Hospital in only ten days during the crisis, the hospital included a cashierless and contact-free supermarket to limit transmission. There are now even Chinese apps providing virtual test driving experiences to help car dealers stay in business as social control measures persist.

China also utilized blockchain technology as a vital tool to weather the crisis. In the first two weeks of February, 20 blockchain-based applications were launched to fight the outbreak, largely to manage citizens’ personal data as they returned to work. The government sent more than $200 million in loans to small businesses through Xuan Changneng, a cross-border, pilot blockchain platform. Chinese insurance firm Xiang HuBao also used blockchain technology to process coronavirus claims more speedily without any face-to-face contact.

Such rapid-fire advances — and the nature of those innovations — could only happen in China. The country is years ahead of the West in the digital financial sector by some measures, and the Chinese government enjoys both an unparalleled ability to enact rapid social mobilization policies and unique access to core operations of industry leaders. Critics say China crossed a dangerous line by using WeChat Pay and Alipay to track people during the crisis, monitoring those who ordered fever medicine online and labeling them as riskier by inserting color codes in their mobile phones. The Chinese example proves that digital financial tools can outgrow their original purpose, sometimes becoming tools of surveillance and social control.

A Delayed Incubation Period

The rapid digital acceleration already seen in China is happening in other countries as well — but at varying stages. Professor Soumitra Dutta, the former dean of Cornell’s business school, describes technological transformations as occurring in three stages: substitution, in which a previous technology is substituted for a new one; diffusion, in which the widespread availability and superior prices encourage wider adoption of the new technology; and finally, transformation, in which the new technology enables fundamentally new ways of living.

In terms of digital payments and interconnected digital ecosystems, China is several years ahead of the West. The country had already undergone widespread diffusion of digital payments and related ecosystems before the crisis, thus enabling the kinds of digital transformations seen at the height of the outbreak there. Western countries, by contrast, are largely progressing through various stages of diffusion. In Italy, where digital payment adoption has been slow even by European standards, and where less than half of people knew in a recent survey what a mobile wallet was, the acceleration they are witnessing amidst a nationwide lockdown is of a lesser stage, though significant nonetheless; digital bank N26 reported a rise in mobile wallet transactions since the crisis, and Italian shoe designers said they were greatly accelerating an ongoing transition from retail to omnichannel businesses.

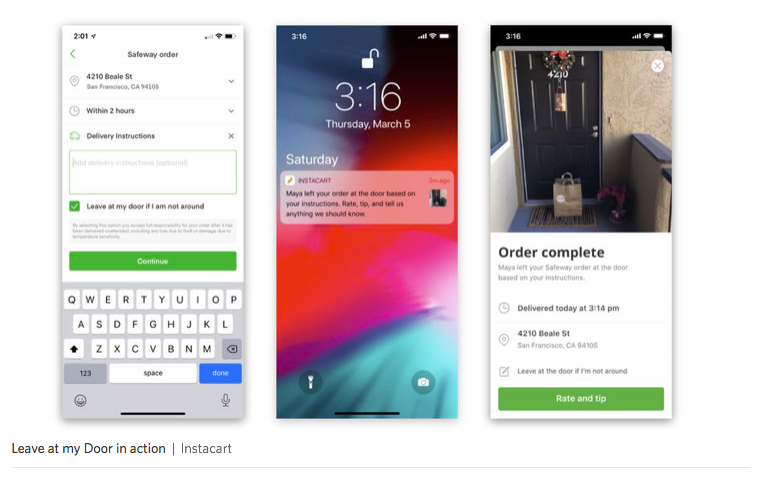

Across the West, the pandemic has accelerated the digital transition in areas like food delivery, trailing China’s footsteps. In light of “hurricane season”-like surges in requests in places like Florida, grocery delivery app Instacart unveiled a contactless “Leave At My Door Delivery” feature that had previously been in beta testing, and Postmates added a similar feature as well, with other competitors considering and implementing similar options.

To better facilitate this transition, banks (and, to an extent, governments) have stepped in with incentives towards the digital. China and South Korea quarantined cash from affected areas as possible vectors of transmission. The Chinese government called for the increased use of mobile payments during the crisis, as did the World Health Organization. Banks across the world in places like Singapore, Vietnam, the U.S. and U.K. are advising their customers to switch to digital banking and mobile payments, offering reduced fees and other incentives. Institutions across the spectrum are sending an overarching message: you don’t need cash -- use your phone instead.

The Black Swan’s Flight Path

Uncertainty reigns during black swan events. One relatively safe bet, however, is the notion that COVID-19 will accelerate countries’ transitions towards a digital economy. Consider, for a start, consumer habits. An ongoing surge in grocery delivery usage in Florida is being compared to surges of hurricane seasons past and raises the question of how sustained such a surge will be. While hurricanes strike Florida once, twice, or perhaps three times a year, a top US health official recently told Americans to prepare for nearly two months or more of shutdowns and teleworking. Whether we like it or not, daily life will change — and decisively in favor of digital tools.

“I think a lot of the behaviors might actually see sustained change over some time. [Consumers] may not have used Apple Pay before… But once they start using it and get more comfortable with it over time, one of the biggest hurdles of consumer adoption is overcome.”

Soumitra Dutta, SC Johnson College of Business at Cornell University

It’s fair to wonder whether such circumstances will force the digitally disinclined to fall in line. Though exact figures are elusive, many millennials are returning home from cities to stay with parents, and some have anecdotally reported teaching their parents how to perform online banking and order groceries through apps. At a critical time of sudden digital necessity, the learning curve for older consumers — those most at-risk by venturing outside — becomes less steep with digital natives stuck back home with them.

But while some older folks may have their children or grandchildren around to help facilitate digital grocery orders, that will not be the case for many. China may have initiated an unprecedented digital transformation in the previous two months, yet they still had to make special exceptions for their elders. Professor Ting Li of Erasmus University, an expert in ecommerce, noted that private sources had shared that in Chinese cities under lockdown, while most reverted to food delivery apps, for the elderly without children to help them online, authorities provided an alternative by keeping corner shops within community gates open for them. Indeed, the elderly are those with the greatest incentive to remain indoors and switch to a contactless, digital-only lifestyle. But if China — with its superior digital ecosystem and unprecedented quarantine conditions — still had to keep commerce analog for the elderly, the same will likely prove to be the case elsewhere.

While both Li and Dutta foresee parallel digital accelerations sweeping across the world, with less advanced regions progressing through stages of substitution and diffusion and more advanced regions experiencing forms of digital transformation, Li believes the gap in digital financial adoption between East Asia and elsewhere may actually widen in the aftermath of the crisis as Chinese unicorns, in collaboration with powerful central authorities, unleash robot deliveries, blockchain contracts, and WeChat Pay-enabled social monitoring. Li argues the cultural attachment to cash and privacy concerns in a place like Germany — the most extreme example of a digital-payments-averse economy, where privacy is so important Uber drivers largely refuse to disclose any personal information down to their car model— may push against immediate incentives to transition towards digital.

“Chinese or Korean practices will sustain, and become even moreso due to coronavirus. To what extent will it likely change practices in the western world? I’m not extremely optimistic about it, to be honest. Will it fundamentally change the behavior moving from cash payments in Germany to all digital payments? I think there’s something deeper rooted in people’s minds that would need to change before you saw real behavioral shifts.”

Ting Li, Rotterdam School of Management at Erasmus University

That is not to say digital acceleration won’t occur in the West or developing markets affected by COVID-19; Li indeed views this event as a potential catalyst for digital finance sectors in a broad sense. But from Li’s perspective, cultural factors do still weigh heavily when guessing how much potential acceleration lies ahead in different regions. By contrast, Dutta believes today’s extreme circumstances have the potential to overcome cultural hurdles. According to Dutta, payments might be the financial sector most primed for a digital acceleration as people become accustomed to carrying out payments and financial obligations from their homes, even in cash-heavy countries.

“You look at India with the demonetization policy about 3 years ago. Suddenly, the whole mobile payment space shot up because cash was far less available. If people are emphasizing that bank notes may be a vector of transmission, or people start finding it more convenient to make digital payments from their home, it might reduce attachment to cash that people have in these societies.”

Soumitra Dutta, SC Johnson College of Business at Cornell University

However and wherever such digital accelerations take place, it is likely to boost several nascent technologes like blockchain, which will greatly aid in the new challenges posed to the global trade and supply chain. Bitcoin’s value so far has crashed during the pandemic, and some reports say the pandemic has delayed China’s research toward its own digital currency, but the former president of the People’s Bank of China suggested the opposite might occur, owing to the digital currency’s efficiency, cost-effectiveness, and convenience in light of the pandemic.

Whatever happens: it is worth entertaining how digital tools can mitigate the risk, both health-related and economic, caused by COVID-19. The crisis is certainly not going away. By the time society emerges from this cataclysmic event, new industries, institutions, and ways of life will have risen from the ashes of the industries, institutions, and ways of old. Think of it, if you wish, as a trial by fire, or a use case by unfortunate necessity.

Image courtesy of Jeremy Stenuit

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

Will COVID-19 Lead To Bigger, Better Borrowing?

Why Western Union Is Still King Of Remittances