Why Western Union Is Still King Of Remittances

~9 min read

P2P cross-border transfers - known as remittances - have long occupied a critically important role in the modern movement of money in emerging markets. The undisputed legacy champion in this field is Western Union, followed by a number of smaller but similar players like MoneyGram & RIA. These players have been celebrated for connecting diaspora populations with their home communities, but they have also been vilified for the outsized fees they collect - particularly along the transfer corridors where diaspora remittances matter most. Disruption-minded fintechs are tirelessly tackling the cross-border challenge, and intend to topple the reigning order with superior convenience, speed, and pricing. But Western Union has weathered it all, contradicting many common assumptions about disruption in financial services.

"Send Money Home"

Cross-border transfers have many different flavors. The most popularly understood definition is the classic remittance case: that of immigrants who send money to their home communities. The very first formal cross-border remittance market was established to handle transactions between the United States and Mexico over three decades ago; it was a cash-to-cash business model composed of money transfer agents on both the sending side and the receiving ends.

Source: Proof of Capital

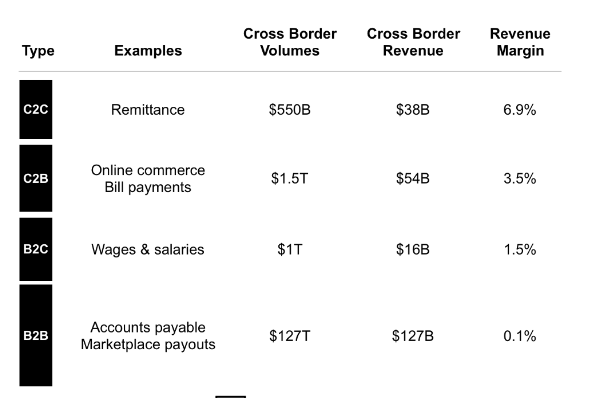

Today, there is no single integrated global remittance market. Instead, there are multiple markets acting as networks connecting various country corridors along which global, regional, and national remittance service providers operate under different legal and regulatory frameworks. An estimated 3,000 such providers charge more than US$30 billion in margin to process approximately 2 billion transactions each year, using a range of traditional and technological methods to initiate and deliver remittances from the “first to the last mile.”

Traditionally, most legacy providers only offered cash-to-cash services before expanding to offer bank account deposits. The newer crop of remittance providers, however, were born digital-only (i.e., lacking physical branches altogether), accept many forms of payment on the send side from debit cards to credit cards to crypto-currencies, and can deliver money into a wider variety of receiving accounts including mobile money accounts - often instantaneously.

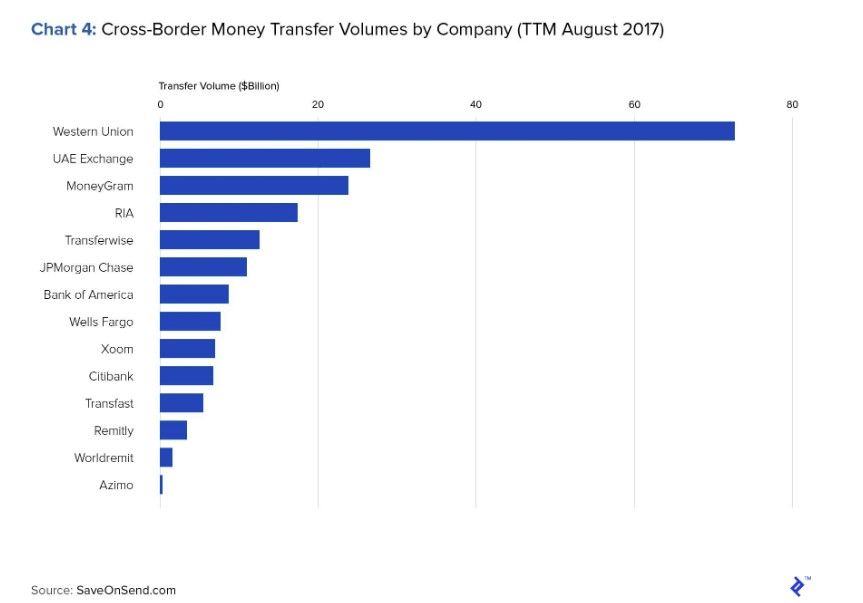

Today, the undisputed leader of the pack in the remittance space is Western Union. It started in the 1850s as one of the first telegraph companies, and through aggressive expansion strategy today commands 10-20% of the nearly $700 billion global remittance market. Western Union’s lasting success has come from an enduring reputation for trust combined with adequate scale to handle anti-money laundering (AML) and local compliance across the globe, plus aggressive pricing strategies that continually evaluate transfer prices across specific corridors, often down to the exact neighborhood and street corner.

It is one thing for a company to attain market dominance in an industry it essentially created, and to survive that industry’s complete dissolution as a result of technological change (which Western Union experienced in the telegram industry). It is quite another, however, for that same company, 169 years later, to not only successfully reinvent itself, but also dominate a separate industry altogether, particularly when the best positioned incumbents in that space include the respective financial giants of each country’s banking system. Indeed, in the age of Silicon Valley startups promising to disrupt the established order, it is easy to overlook how thoroughly a firm like Western Union must have reconsidered its business model in order to attain the comfortable position it enjoys today.

Different players have historically picked off specific corridors to compete with Western Union in. MoneyGram and Ria, for example, leverage their unique brand relationships and knowledge of specific ethnic groups (for example Filipinos or Mexicans in the US who send money to specific parts of their home countries). But these players from the ‘old-guard’ have historically followed the same playbook as the market leader - ethnically-targeted branding paired with aggressive price competition in over-the-counter transfers. In other words: bring cash, pay a fee, and wait for your folks back home to confirm they have cash in hand.

Startup Upstarts

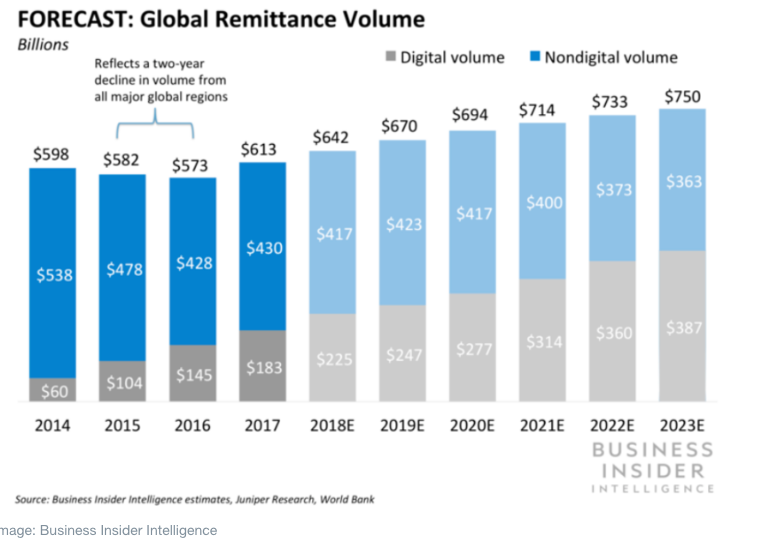

With respect duly paid to the elder statesmen, it’s also worth noting that Western Union’s global market share is slowly eroding, while its old-guard peers have also struggled to adapt to the broad trend sweeping every industry on the planet: digitization. Indeed, for the first time in history, digital channels are projected to overtake traditional ones, in terms of value of money sent cross-border, within the decade.

It's a fair assumption that the pains of digitization experienced by bloated institutions are hardly relevant to the spry fintechs like TransferWise, Remitly, or WorldRemit who seemingly emerged fully formed from the internet over the past decade. These companies have various specific strategies for gaining market share, but what unifies them is an overwhelmingly digital-only experience on the ‘send’ side, and a focus on convenience, flexibility, and transparency around pricing. On the receiving side, the options are usually wider as well - encompassing not just bank account transfers and cash-pickup, but deposits into select mobile money wallets as well as direct airtime purchase.

Local dynamics often prove the deciding factor when it comes to whether users will embrace a new fintech solution or stick to a legacy service. For instance: WorldRemit’s only mobile money wallet recipient in Senegal is Wizall, an up-and-comer fintech just now expanding across francophone Africa - in other words, one whose presence is far from universal even in Senegal, its operational stronghold. Other local competitors vying to build a mobile money ground-game for domestic transfers and payments, like Wave, may be the right choice for a specific community geographically, but alas, their service has not yet been onboarded onto WorldRemit’s platform. In a low-trust financial environment like Nigeria, it's even tougher sledding; WorldRemit’s only mobile money partnership is with Paga, an early-stage mobile money player whose strategy has focused on creating a large agent network to handle cash-in / cash-out (CICO) functions, given the low acceptance of mobile wallets among Nigerian users. Despite the partnership announcement in Q2 2019, however, it’s not clear whether that delivery route is currently operational.

Despite the dynamism of options on the fintech side, the old-guard is not going anywhere just yet - particularly since they have held their own with the pace of digital change. Although Western Union has been forced to shed swathes of staff to consolidate its operations, it has invested in a string of forward-looking tech partnerships which have enabled integrations into Whatsapp, WeChat and Safaricom’s mPESA. Likewise, MoneyGram has received a sizeable injection from blockchain player Ripple that has reassured investors its future is fintech-friendly.

Margin Mayhem

And now, for the elephant in the room: traditional remittance providers like Western Union and MoneyGram are typically more expensive than their fintech counteparts, to the tune of an estimated 15% premium on average. Chalk it up to being a trusted brand for immigrants and their families. These premiums can be built in as a transfer fee, a marked-up foreign exchange rate, or both. Depending on the corridor, these fees could account from almost zero to up to 20% of the total transfer, essentially determined by the competitive positioning of fees in the corridor vis a vis other market players.

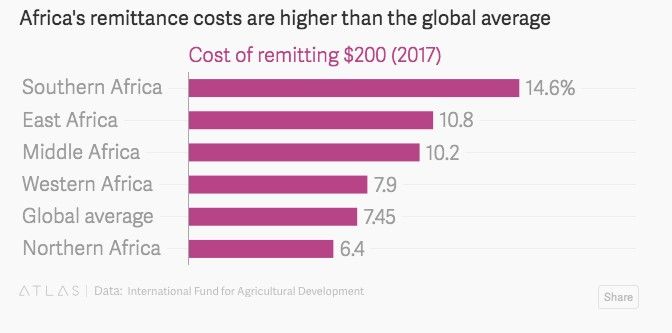

This dynamic, though logical from a market perspective, obviously doesn't benefit the workers and families who depend on remittances to make ends meet. The cost of remitting to Africa has historically been among the highest in the world, averaging around 10% of the total amount sent. Given the well-documented pro-poor impact that remittances have on financial inclusion, rural youth development, and even industrialization, the international community included a target in the Sustainable Development Goals of averaging 3% on fees for remittances. Remittances already constitute more than triple the value of foreign assistance via ‘aid’, and they eclipse the value of foreign direct investment (FDI) in many emerging markets.

Source: Quartz

Reduced fees on international transfers thus represents a massive opportunity to directly improve the lives of the most vulnerable - something fintechs claim they are doing much more effectively and quickly than their legacy counterparts. Ultimately, the average cost of sending money has indeed been dropping, in part thanks to the lowered costs of operation unlocked by digitization, which is in turn driven by a steady surge of VC funding for fintechs eager to make their mark on the remittance space.

Corridorization

Like so many topics in digital financial services, adoption is tricky when it comes to digital remittances. So far, the propensity to use a fintech that leapfrogs the ‘analog’ way of cash appears highly corridor-specific.

Indians living in the US, for example, are disproportionately employed in the IT sector, and thus are not only relatively highly educated, but also very confident evaluating different remittance providers online. This behavior devalues the ‘trust premium’ which Western Union commands among the less digitally-literate - resulting in a share of transfers performed online above 80%. For Filipino senders from the US, however, the average use of digital for money transfers is estimated at less than 10%.

What we can learn from this spread, as well as the stability of the price premium which incumbents maintain among lower-educated groups, is that trust and habits matter tremendously, and that competition for relationships continues to be fierce. The ability to offer a locality-compatible solution is so important, in fact, that lesser-known players have been able to capture market share from the old-guard titans in certain corridors where their product is "just right". Mukuru in Southern Africa, for instance, operate just 51 branches in total but own 20% of the South Africa - Zimbabwe corridor.

"Fintechs have historically been more proactive seeking integrations given their lack of brick and mortar cash-out points, but the 'old guys' are picking up, and we at Wizall welcome any partnership that lowers fees and improves experience for our customers."

Quentin de Ravignan, Products & Partnership at Wizall Money

Part of the secret to success for the growing crop of hyper-localized cross-border providers is having a low-cost, digital-first sending infrastructure, combined with seamless integration into existing mobile money infrastructure on the receiving end. This matters because the ‘ground game’ of agent networks and pay-out infrastructure varies village-to-village. The good news is that in such dynamic environments, the opportunities to continue picking off market share from recognized leaders will only grow as mobile money usage increases.

At the same time, it’s important to note that the value of informal transfers - those sent through friends, family, hawala, or specialized border crossers - may be up to 10x that of formal channels, driven again by trust issues (but also through lack of access to the documentation required for AML compliance). Sometimes, migrants would rather send the ultimate goods rather than cash - thus preferring informal networks for sending items like consumer goods and food to the remote communities where traditional couriers don’t go. In such circumstances, and in similar ones even when money itself is being sent, senders may prefer informal routes simply on the basis of the exorbitant costs of the formal channels.

The consequent risks associated with such informal routes are hard to quantify, but on average are likely higher than formal channels. This means that as long as the costs of the formal sector keep dropping, financial inclusion widens, generational trends drive widespread digital literacy, and intra-African remittances grow, the formal channel market will expand and the ground will continue to shift under the incumbents.

Outrunning A Rising Tide

Nobody doubts digitization is the future of remittances. But a dose of reality should temper Silicon or Savannah Valley techno-optimism forecasting that systemic disruption from the status quo is just around the corner. Massive swathes of the world are not ready or able to go digital with their money habits - particularly at a time when global stability is far from assured as markets reel from COVID-19.

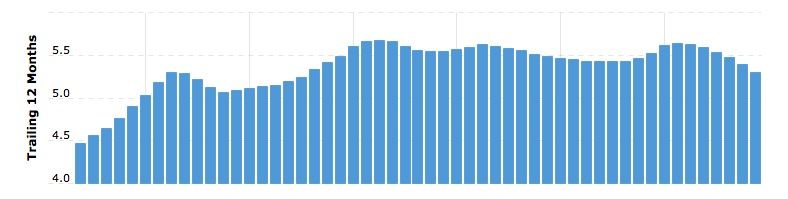

As long as leaders like Western Union continue to innovate just enough to keep pace with the trends, however, it is likely they’ll continue to secure their position at the top of the remittance market, and it is certainly clear to them that their principal source of growth is coming from digital-sending. Western Union, specifically, with annual revenues hovering around $5 billion over the past decade, has survived over a century and a half in business, and with a solid chunk of Millenials among their digital user base, has no plans of fading into obsolescence anytime soon.

Western Union Revenue 2006-2019: Large, Historically Flat, & Staving Off Decline

Source: Macrotrends.net

They may not be in a rush to kill the cash cow that has made them the king of the hill, but they must also be wary of dying a slow death by a thousand cuts; after all, the collective market share of fintechs like TransferWise, Xoom, Remitly and WorldRemit grew from only 2.5% in 2015 to 12% in 2018. Facing the growing challenge from fresh-blooded fintechs, the old-guard must realize, like the famous last prince of Italy wrote of the dying aristocratic order at the same time of Western Union’s birth in the mid-19th century: “everything will have to change if they are to stay the same.”

Image courtesy of Alistair MacRobert

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

Digital Finance Is As Important As Ever During COVID-19

Better Payments, Better Apps: The Sharing Economy Wars