Device Financing: The Phone Is Not The Product

~10 min read

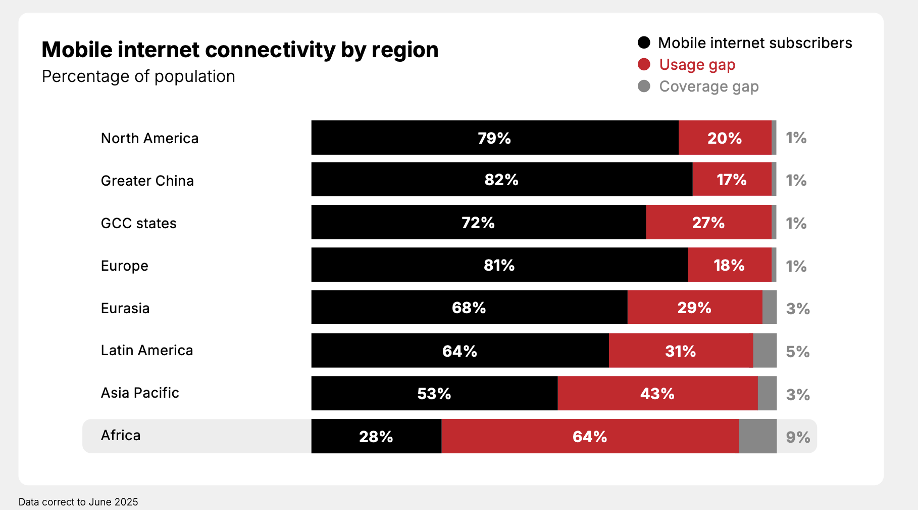

In Sub-Saharan Africa, an entry-level Internet-enabled smartphone costs the average person in the poorest quintile the equivalent of 87% of their monthly income, according to data gathered by the GSMA. That single statistic does more to explain the global digital divide than any infrastructure map. The coverage problem has largely been solved: 96% of the world's population now lives within reach of a mobile Internet network. Yet 3.1 billion people who live within range of mobile Internet do not use it. The bottleneck, experts from the GSMA and elsewhere are finding, is the device. Device financing is subsequently emerging as the most viable pathway to build credit identity for the unbanked — but its economics impose a hard floor that risks excluding the very populations it aims to serve without intervention.

Source: GSMA

Source: GSMA

How Low Can You Go?

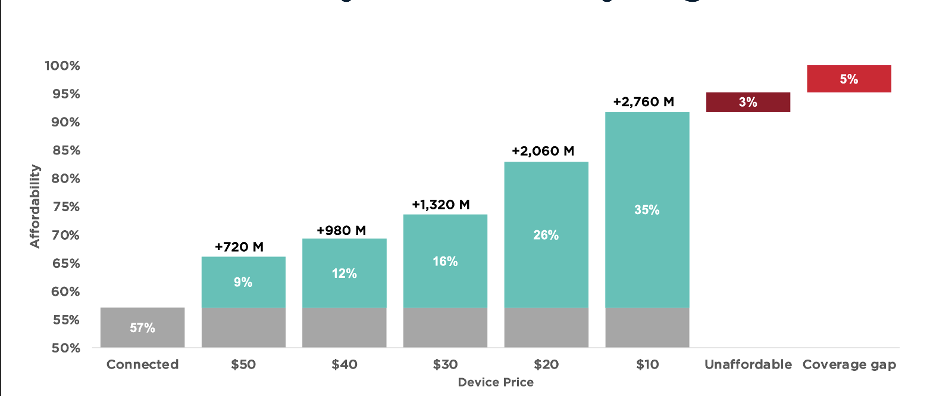

Despite years of effort to engineer down the cost of an Internet-enabled handset, the economics of hardware manufacturing have run into a floor that policy and financing alone cannot dissolve. The GSMA's Handset Affordability Coalition — involving the World Bank, the ITU, and the WEF Edison Alliance alongside major mobile operators and OEMs — has spent years working toward a $40 4G smartphone viable for the markets that need it most. That seems to be finally coming to fruition, as seven manufacturers are now in active one-on-one commercial negotiations with G6 operators, with six African pilot countries announced at MWC Barcelona 2026 and more expected to be revealed at MWC Kigali in June.

But a $40 device, if it arrives, still will not reach the bottom of the pyramid.

“We need to get a handset cost down to maybe even $10. And right now, that doesn't exist for Internet-enabled handsets.”

Claire Sibthorpe - Head of Digital Inclusion, GSMA

Taxation compounds the hardware problem. Import duties and luxury levies on smartphones can add up to 30% to the retail price of a device in some markets, according to GSMA — a burden that falls entirely on the consumer least able to absorb it. South Africa's decision in 2025 to scrap a 9% luxury excise duty on smartphones below 2,500 Rand was one encouraging policy development — but it remains the exception, not the rule.

Potential impact of a reduction in device prices on mobile connectivity - Affordability target of 20% of monthly GDP per capita

Source: GSMA

Source: GSMA

But even the prospect of a commercially viable $40 phone remains contingent on a fragile coalition of compromises between parties whose commercial interests only partially align. For device financing companies, the hardware price floor creates a binding constraint on business model design. George Thekkekara, Chief Risk Officer of Yabx, which partners with mobile network operators and banks across emerging markets to provide AI-driven underwriting and loan management on installment plans, is candid about where the economics break down.

“I would draw the line at around $70 — that's probably where we can operate: $60–$70. But I think even that is not easy. Making the economics work for all parties is difficult when there are many mouths to feed.”

George Thekkekara - Chief Risk Officer, Yabx

A $30 or $40 device, he argues, offers insufficient value to justify the telco's distribution investment, the bank's credit risk, and the fintech's operational overhead simultaneously. This creates a structural dead zone: below about $60, devices become affordable — but no longer financeable.

The Ecosystem Play

Across Africa, more than half of all mobile connections are still on feature phones. The migration to smartphones is therefore not just a consumer upgrade cycle — it is the central commercial interest of every mobile network operator on the continent. Device financing companies have exploited this alignment to construct what might be called development-oriented platform network effects: closed loops of data, distribution and collections built around the telco relationship, substituting for the public infrastructure that mature credit markets take for granted.

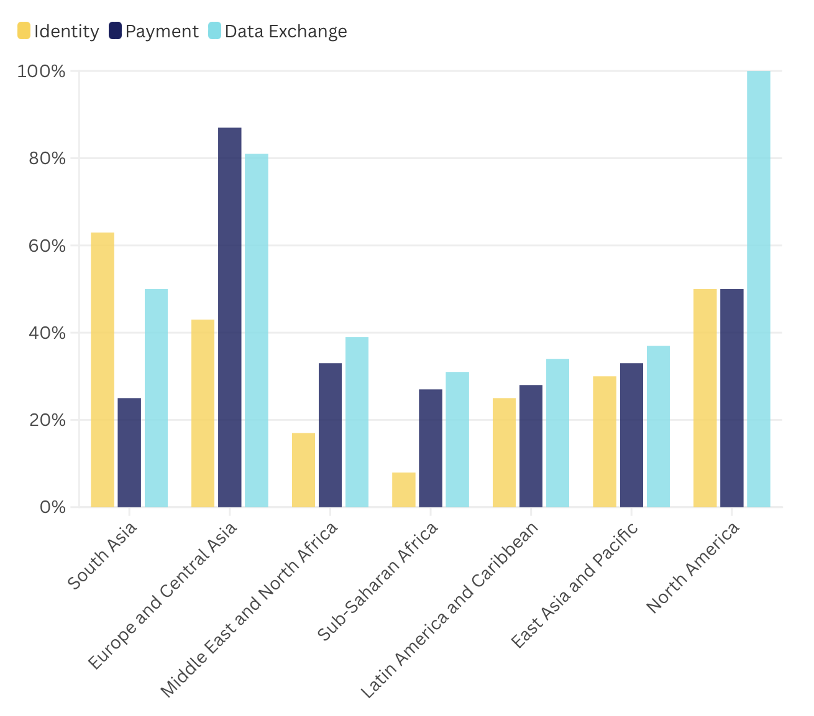

In a market with mature Digital Public Infrastructure (DPI) — a robust identity layer, real-time payment rails, and functioning credit bureaus — a lender can acquire customers from the open market, underwrite them using bureau data, disburse through any bank account, and collect via automated standing instructions. This is, broadly, how consumer lending operates in India, where Aadhaar biometrics cover 1.3 billion people, UPI processes tens of billions of monthly transactions, and formal banking inclusion has risen from 25% to over 80% since 2008.

Africa is not India. Its DPI infrastructure is still being built, piecemeal and unevenly, across dozens of sovereign jurisdictions with widely varying regulatory environments. Credit bureaus are thin or absent. National identity systems are incomplete. Automated cross-bank collection rails do not uniformly exist. In this environment, the telco ecosystem substitutes for what state-built infrastructure provides elsewhere — and the device financing companies that have thrived are those that recognized this earliest.

Prevalence of systems meeting DPI criteria across global regions

Source: ODI Global

Source: ODI Global

“In a market like India, you could just go open market and give credit to people. You don't really need the ecosystem because the DPI infrastructure is the ecosystem. That is not there in Africa — it's an incomplete DPI infrastructure. That is why the ecosystem strategy is a key way to overcome the limitations.”

George Thekkekara - Chief Risk Officer, Yabx

The telco relationship solves multiple problems at once. It provides a pre-qualified customer base: people already active on a network, and with a behavioral track record. Telco and mobile money data provide daily-frequency signals far richer than those of a traditional credit bureau. And telcos provide distribution infrastructure in the form of physical stores, agent networks and direct-to-consumer communication channels. Lastly, it provides a collection mechanism, since repayments can be debited directly from the mobile wallet.

Yabx has built its underwriting architecture around three data layers: telecom metadata, mobile wallet transaction flows and app-level behavioral data for smartphone holders. But the most distinctive element of the model is a fourth variable almost no one else is modeling explicitly: loyalty.

“If a customer is not keen on continuing their relationship with their network provider, you might be a good customer, but you might churn off that network. Given the nature of our product, it becomes very difficult to collect from you.”

George Thekkekara - Chief Risk Officer, Yabx

A borrower who switches mobile networks mid-loan severs the collection mechanism entirely — the mobile wallet becomes inaccessible, and the communication channel goes dark. Modeling churn risk as a credit variable is, in effect, treating the telco ecosystem itself as collateral. It is a form of platform lock-in that happens to produce better repayment outcomes.

This creates a self-reinforcing flywheel. As Yabx's portfolios mature, the models improve; as the models improve, eligibility rates rise; as eligibility rates rise, the telco's distribution investment is justified. After four to five years of operation, Thekkekara reports that nearly two out of three eligible customers qualify for a product — a rate that keeps MNO partners commercially engaged without demanding the kind of blanket approvals that would destroy portfolio quality. Navigating that needle has been the central operational challenge of the industry.

PayJoy, which finances smartphones for unbanked consumers using device-locking technology embedded directly at the OEM level, has solved the same problem from a different angle. Rather than building deeper into the telco ecosystem, PayJoy licenses its security platform directly to OEMs, embedding it at the manufacturing stage — going below the operating system toward the chip level, building a moat that is technically difficult for competitors to replicate and that allows it to offer, by its own account, the lowest jailbreaking rate in the industry.

“Replacing costly collections processes with automated mobile security software, and replacing costly human underwriting processes with AI-driven machine learning — those were the two core technology innovations that made us profitable.”

Doug Ricket - CEO, PayJoy

The common thread between both approaches is the transformation of the smartphone itself into collateral — something that didn’t previously exist in consumer lending for this demographic.

Striking The Right Balance

Device locking remains the mechanism that separates smartphone financing from every prior attempt to extend consumer credit to unbanked populations at scale — and the feature that makes regulators uneasy.

The industry has converged on graduated locking as both a risk management tool and a consumer protection principle. In the case of Yabx, the borrower's "most favorite app" is restricted first, then progressively broader Internet access, with full device lock reached only around day 28 or 30 of delinquency — and even then, the repayment pathway is built directly into the locked device. Phone calls and, critically, mobile money access are maintained throughout. "Those really essential services," notes GSMA's Sibthorpe, "don't need to always be locked."

Yabx estimates that roughly 70–75% of borrowers pay without any intervention, while most of the remaining borrowers respond to digital nudges, like reminders and graduated restrictions, before a full lock becomes necessary. Mobile wallet auto-debit adds another collection layer, allowing outstanding installments to be swept from incoming wallet balances with customer consent. For the small fraction who reach 90-days-past-due, human collections teams and credit bureau reporting follow.

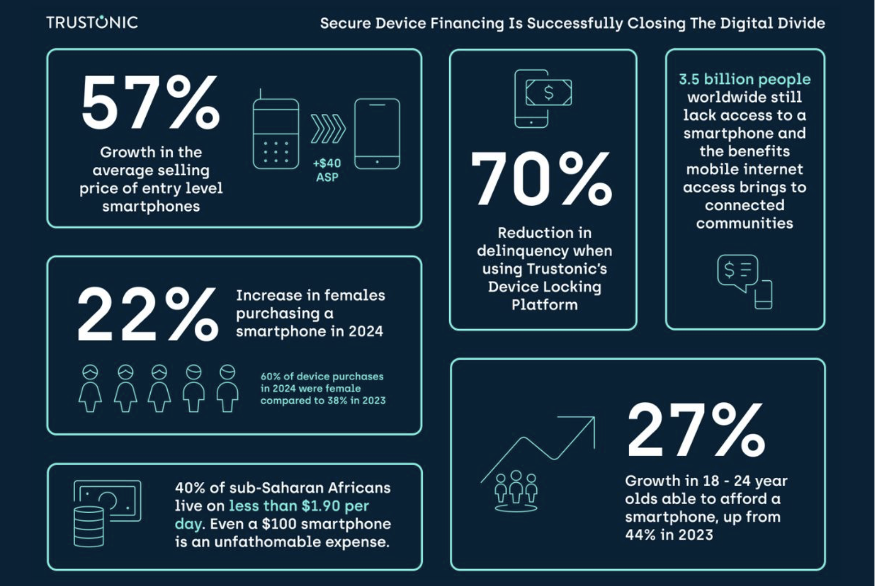

Source: Trustonic

Source: Trustonic

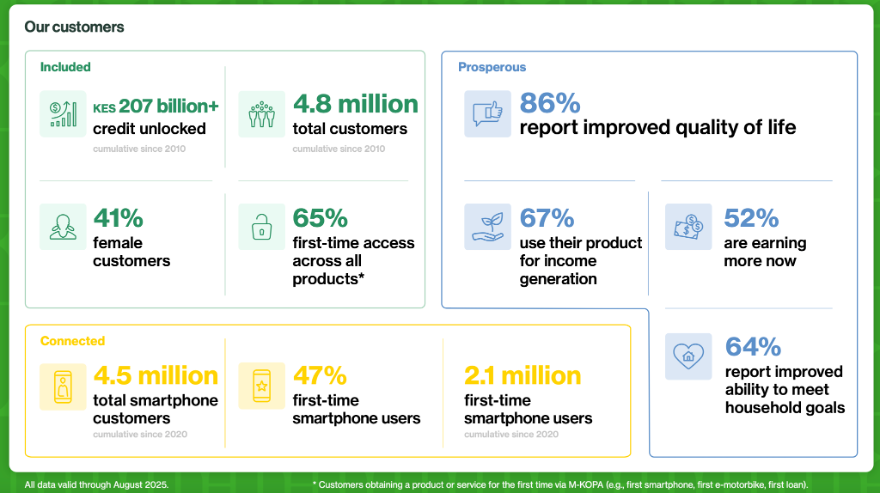

The lock is not a punishment; it is what makes credit possible at all for people otherwise excluded from it. But the ethical tension is real. The same alternative data that enables inclusion can also enable discrimination. GSMA's Sibthorpe flags algorithmic bias as a risk requiring active testing when facilitating device financing. The irony runs deep: women, who are disproportionately excluded from formal credit by both traditional and algorithmic scoring, turn out to be systematically better repayers than men, a finding confirmed independently by M-KOPA, which has financed over $1.5 billion in credit to more than 6 million customers. M-KOPA has even begun to pivot its acquisition strategy toward women borrowers explicitly.

“Women are often better repayers of these things than men. Some of these alternative data sources are very valuable for women who don't have formal credit histories.”

Claire Sibthorpe - Head of Digital Inclusion, GSMA

Yabx voluntarily applies GDPR standards, deploying all processing within the telco's own network perimeter and using only tokenized, non-PII transaction signals in its models. PayJoy offers customers full transparency and opt-in/opt-out control over data sharing, while maintaining a technical separation between the security lock and any data collection.

But few regulations are on the books in poorer countries to mandate such practices. Kenya's Digital Credit Providers Regulations represent the leading attempt at a formal framework, requiring CBK licensing, data protection policies, and consumer redress mechanisms from digital lenders. No continental African standard yet exists, and GSMA notes that some countries prohibit device locking outright, rendering PAYG financing legally inoperable without workarounds.

From Device to Financial Identity

The smartphone loan was never really about the smartphone. PayJoy recognized early that the deeper problem wasn't smartphone financing specifically — it was that credit, in general, was not available.

“We expanded our mission from just smartphones to solve the bigger problem of credit”

Doug Ricket - CEO, PayJoy

The company now offers a PayJoy Card and unsecured cash loans across its 20-million-customer base in nine countries across three continents. Ricket says the phone loan serves as the acquisition and KYC instrument, and the credit track record generated during repayment serves ultimately as the asset.

Yabx's Thekkekara frames the same logic from a different direction. The device loan is the entry ramp to an asset financing journey.

“You have to give smaller ticket products and build that financial identity and credit history. But once they reach a certain point, their credit needs evolve.”

George Thekkekara - Chief Risk Officer, Yabx

The vision — not yet realized, but directionally clear — is a credit line that decouples entirely from the phone: a facility that can be integrated with Visa or Mastercard, used for other purchases, and managed over time as the customer's creditworthiness compounds. In this model, the phone is the first step of a much longer financial journey.

The inclusion cascade this model produces is already measurable. Of M-KOPA’s customers in Kenya, 47% are first-time smartphone owners, 37% accessed their first formal loan through M-KOPA and 68% received their first health insurance coverage, according to M-KOPA figures.

Source: M-KOPA Kenya Impact Report 2025

Source: M-KOPA Kenya Impact Report 2025

This graduation logic is also where the impact capital question becomes acute. The purely commercial model works at ticket sizes of $70 and above. Below that, the mathematics break down — not because the need isn't there, but because the cost structure of origination, collections, and risk management cannot be recovered from a loan of $30 or $40. Bridging that gap likely requires the participation of development finance institutions and impact-oriented funds willing to accept below-market returns in exchange for inclusion outcomes. The GSMA's Handset Affordability Coalition positions DFI backing as the mechanism to unlock that final segment, estimating that a properly structured de-risking arrangement could bring Internet access within reach of an additional 20 million people.

The Platform Stakes

The deeper question hanging over this industry is one of durability. The telco ecosystem model — substituting for absent DPI — is a salient workaround to the problem, but it will become less necessary as the underlying infrastructure matures. As African countries progressively build out national identity layers (nine of the eleven countries implementing India's MOSIP open-source identity platform are in Africa), interoperable payment rails and credit bureau coverage, the moat that surrounds ecosystem-based lenders will narrow.

When open-market lending becomes viable — in which a lender can reach any customer through any bank account, pull any credit bureau and collect through any payment rail — the competitive advantage currently held by those who have stitched together telco partnerships, OEM relationships and proprietary data flywheels will face serious commoditization pressure. The race, therefore, is to build credit histories and customer relationships deep enough to survive the DPI transition.

PayJoy, for its part, is already moving down the stack — literally, toward chip-level security integrations with smartphone manufacturers — and across the product spectrum, with ambitions of financing laptops, appliances and vehicles using the same secured-asset protocol it pioneered with phones. Yabx is piloting a generative AI-based digital assistant for collections — a first-layer intervention that replaces human call center outreach for early-stage delinquency.

Neither of these innovations changes the fundamental question: will the platforms being built now remain open enough to serve the poorest 20%, or will financial inclusion calcify into a new form of gatekeeping — one defined not by bank account balance, but by telco loyalty score?

The question is not whether device financing can build credit identity — it already is. The question is who controls that identity, and on what terms.

Image courtesy of Eirik Solheim

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

When Your Identity Is Gone - And There's No One To Call

How DPI Determines the Shape of Sovereign AI