Digital Lending’s Self-Regulation: A Redemption Story?

~9 min read

For years now, digital lending in emerging markets has faced public rebuke for at times utilizing deceptive marketing tactics, predatory interest rates and abusive debt collection practices, including from Mondato. Yet despite years of back and forth between government and industry stakeholders, most of the leading digital lending markets are still bereft of comprehensive regulatory schemes catering to the unique characteristics and needs of the digital lending market. Almost a year and a half into the pandemic, however — and following the fraught challenges the crisis posed to lenders, as Mondato described last year — public scrutiny and market maturation is compelling positive steps towards reforming the digital lending landscape among digital lenders themselves. A look at three of digital lending’s leading markets — Kenya, India, and Indonesia – reveals intriguing patterns in digital lending’s evolution during COVID times, alongside unique characteristics distinguished by each market’s demographic, technological and regulatory differences. As comprehensive regulatory frameworks continue to face indefinite delays, can digital lenders self-regulate and bring their own industry to heel?

Listening To The Critics

In spite of years of discussions and bills being debated, there have been no comprehensive regulatory regimes established in Kenya, India or Indonesia directly pertaining to digital lending; it was only last year that South Korea became the first country to implement laws solely dedicated to digital lending. Yet after years of public outcry, private sector initiatives have taken the lead in reining in bad actors who prey on consumers.

Kenya’s digital lending space was among the world’s first to explode, contributing to the country’s rapid financial inclusion increase from 26.7% in 2006 to a remarkable 82.9% in 2019. Yet unbridled growth also wrought dangerous increases in consumer debt levels and worsening financial health outcomes amidst predatory practices in the industry, as the Insight previously discussed.

In the Kenyan context, COVID culled many digital lenders from the space, which saw skyrocketing default rates — as Mondato previously warned — exacerbated when the Central Bank of Kenya prohibited digital lenders from reporting delinquent borrowers to the credit bureau, which incentivized consumer defaults further. While the crisis eliminated much of the small, local digital lenders who were not financially prepared for the economic shock — unlike the larger, well-capitalized foreign lenders — not all bad actors were excised by COVID pressures, according to Kevin Mutiso, CEO of Alternative Circle and Chairperson of the Digital Lenders Association of Kenya. The pressures of the COVID economy only encouraged more aggressive practices by rogue actors, said Mutiso, with hidden fees and public shaming on the rise.

“The ones that have survived have just continued making a mess of things and have actually created a more dire situation as defaults increased. There has been quite an outcry from the public regarding some of the debt shaming practices, and ever since I started, it’s never been this bad. I think I’m getting 10-15 notifications on e-mail, WhatsApp, etc. letting me know that this player is doing that, this company is doing this… it’s never been this crazy.”

Kevin Mutiso, Chairperson, Digital Lenders Association of Kenya

Despite the market turbulence, long-promised regulations are yet to come to fruition in Kenya, with the country’s data protection laws just recently being operationalized. Amidst growing outcry, Mutiso’s Digital Lenders Association of Kenya (DLAK) became a primary force during the pandemic to reform some of the industry’s worst actors.

Like digital lenders associations elsewhere, Mutiso’s DLAK allows the industry to standardize a code of conduct to follow, with violators risking ostracization and reporting to authorities, which DLAK has forged ties with. Last year, Kenya’s DLA began a public awareness campaign to shame the rogue actors publicly shaming late borrowers, airing YouTube ads for three months to inform the public of companies employing unethical tactics. According to Mutiso, this campaign brought such rogue actors to the negotiating table; with the association currently comprising approximately 75% of the entire Kenyan digital lending market, Mutiso and DLA’s campaign has forced promises by rogue actors to end their habits like public debt shaming and deceptive marketing tactics by the end of this month. Planning to observe these companies during an ensuing six-month trial period, after which these companies will become DLA members, Mutiso estimates up to 90% of Kenya’s digital lending market will fall under the association’s self-regulatory umbrella and its enumerated code of conduct; two rogue lenders remain uncooperative.

As the association’s efforts continue, Mutiso believes the actions of the association have done much in repairing relations and trust with the public, with customers now well-aware of the dichotomous nature of companies in the market — between those expanding financial access, and those preying on the vulnerable.

Follow The Leader

Digital lenders associations also play a critical role in the maturation of the sector in India and Indonesia, two of the fastest-growing markets in Asia. In the case of Indonesia, where peer-to-peer lending comprises such a large segment of the wider fintech industry that “fintech” is often used interchangeably to refer to “digital lending,” the regulatory authority, OJK, currently only has on the books a basic 2016 law created in the industry’s infancy, a time in which regulators knew little of the nuances and challenges of digital lending. According to Indonesian lawyer Maria Sagrado, who participated in discussions regarding the drafting of the 2016 law and has overseen much of the deal-making in Indonesia’s fintech space, OJK made the local digital lending association, AFPI, mandatory for all legally operating digital lenders to be a part of. Crafting a quasi-regulatory sandbox, regulators deputized AFPI as co-regulators to create a series of policies and standards for local operators to follow.

“Even without new regulations yet, the AFPI tries to regulate these [sectors]. There are various policies by AFPI to follow. So the new regulation hasn’t been issued, but it doesn’t mean that the 2016 doesn’t really cover these things. [OJK] is still trying to control it through this association.”

Maria Sagrado, Indonesian lawyer

Aided by AFPI’s oversight, thousands of illegally operating companies were shut down in recent years by the OJK, which has reportedly improved market conditions recently, though the market still deals with predatory and illegally operating companies. While AFPI’s policies are broad, they aren’t exactly stringent, as evidenced by the association capping daily interest rates at a still high 0.8%. To add to that, some companies don’t always apply in practice what they agree to on paper, according to Sagrado.

Source: Boan Sianipar

Indonesia’s market, which has been so flooded by digital lenders the OJK put a moratorium on granting new digital lending licenses, has also dealt with a horde of companies originating from China employing abusive practices. China’s crackdown on P2P lenders in 2017 didn’t shut up shop for these predatory lenders — it simply pushed their activities abroad. In Kenya, India and Indonesia, some of the most predatory companies originate from China, with such entities often using different company names as before, according to Sagrado.

How they have fared of late tells much of the progress each market has made in handling predatory actors. Two of the rogue actors, Okash and Opesa, that Kenya’s DLA publicly shamed on YouTube – and eventually brought to heel — were Chinese-owned. After struggling with hordes of Chinese-run companies applying a high-interest, high-default business model last year, India has also recently managed to finally stop these predatory — and often illegally operating — digital lenders. According to Yogi Sadana, CEO of Indian digital lending app CashE and co-founder of India’s Fintech Association for Consumer Empowerment (FACE), which is comprised of digital lending companies, the scourge of abusive companies mostly subsided in this past financial quarter after Google agreed to remove over 200 lending apps from its store in January, coupled with digital lenders associations’ increasing ability to create public awareness and establish industry standards.

“There was an opportunity [last year] where a lot of lenders were not lending, their policies were tightened, so it gave a bit of space for these [bad] lenders to operate. But since a lot of tightening has happened from the banks, the regulators, the enforcement agencies, and the consumers are more aware about this, we haven’t heard too much in the last few months.”

Yogi Sadana - CEO of CashE, Co-founder of FACE

Bring In The Feds

For all the gains private sector endeavors have made in self-regulating these expanding digital markets, digital lenders associations agree on the need to create robust regulatory mechanisms to institutionalize standards and foment further trust among consumers. In the case of India, because banks and non-banking financial companies fall under the Reserve Bank of India’s regulatory purview, Sadana views this preexisting regulatory regime as effectively creating a regulated yet enabling environment for digital lenders, evidenced by their contributions in cracking down on bad actors; at the same time, observers have noted some blind spots like fintechs’ proprietary platforms, which are only indirectly regulated by the RBI. The RBI employed a working group beginning in January to study and recommend further regulations in the digital lending space, although it is uncertain when regulations are forthcoming.

In the case of Indonesia, proposed revisions to the government’s 2016 law have been swirling around for at least a couple years. The drafted regulations, which are still evolving, would potentially adopt general principles of the EU’s GDPR data privacy regime — a critical missing ingredient in all these markets’ efforts to better safeguard customers’ data, which can otherwise be surreptitiously exploited for monetization or public shaming purposes — and ensure more transparency requirements among Indonesian lenders. Although legislators have signaled more urgency in the past year, it remains unclear when amendments to the bare bones 2016 regulation will actually come to pass — and what role AFPI will have moving forward in self-policing and promoting good corporate governance, which remains the preferred option for most of the industry, according to Sagrado.

When these regulations will be actually implemented is the real question that nobody knows. In Kenya, Mutiso is currently engaged with lawmakers over the contents of the long-awaited 2021 CBK Amendment Bill. The bill, which has already been discussed for a couple years now, is more than a year away from actually being passed and implemented with all the necessary enforcement mechanisms, according to Mutiso. Mutiso is working with lawmakers to implement consumer practice guidelines on areas like marketing techniques, debt collection practices, and consumer protection guidelines — essentially codifying what DLAK has been doing on its own. Taking regulatory cues from elsewhere like India, whose regulatory regime is furthest along of the three, the DLA of Kenya is working to include a financial ombudsman in the law to arbitrate issues between lenders and customers. To create a more enabling environment, Mutiso is also pushing to insert predetermined timelines for obtaining licenses, a process which can currently linger for months. While mending a still-fragile relationship between lenders and lawmakers, the DLAK is arguing against some measures currently in the bill, such as requirements for the Central Bank of Kenya to approve all products and pricing in the market, which Mutiso views as encroaching on business decisions.

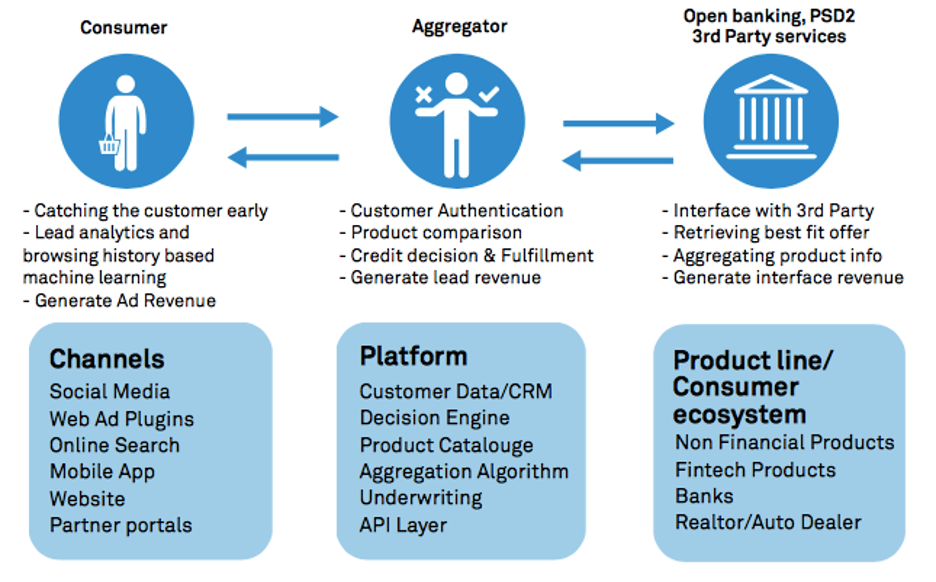

In spite of the regulatory delays, however, the relative success of self-regulation inspires optimism for multiple paths to solve some of the sectors’ issues in areas of financial health and consumer protection. Alternative credit scoring’s emphasis on loan applicants’ “willingness to pay” over “ability to pay” expanded financial access in a revolutionary way — but at the cost of vulnerable customers’ financial health. While COVID exposed the systemic pitfalls of algorithmically emphasizing a “willingness to pay,” deepening data sets and strong AIs can broaden beyond this initial scope while incorporating ability to pay factors as well. In the case of Sadana’s CashE, the company saw a small rise in defaults last year, but the company’s adaptive algorithm, aided by India’s sophisticated UPI-based tech stack and factoring in the ability to repay, has since managed to adapt to evolving COVID conditions. Such functionality only promises to improve with the introduction of account aggregators to India’s infrastructure. While account aggregators, which will unify individuals’ financial information to be safely and securely shared with third parties, are in the early stages of implementation, according to CashE’s Sadana, they will offer the potential for a more agile loan application process and a fuller, more holistic picture of an applicant’s financial standing.

Source: WIPRO

The promise of open banking stretches across these nascent markets. As Kenya DLA’s Mutiso views it, deeper data sets present an opportunity for the next evolution in digital lending.

“Digital lending solved so many issues around financial inclusion, and the main one was data aggregation. We started with willingness to repay because it was the lowest-hanging fruit. So now we are moving to ability to repay, which means going deeper into the data sets that are available to us. When you think about deeper sets, you now start moving into the realm of open banking — open APIs, controlled pricing, and the rights of the data subjects.”

Kevin Mutiso, Chairperson of Kenya’s Digital Lenders Association

As Mutiso noted, Kenya’s government, which only recently operationalized its 2019 data protection law, has sent positive signals regarding open banking, which would allow for a more unified understanding of a person’s financial standing. Under the proper legal protections, more data means more access, yet more responsible, sophisticated lending — which will likewise lower interest rates.

Private sector improvements notwithstanding, it’s important to remember that not even the digital lenders associations view self-regulation and private sector actions like Apple and Google’s removal of predatory apps as sufficient oversight mechanisms. Association and company rules on paper are not always observed in practice, like in Indonesia. Illegal companies operating under the radar linger without official regulatory bodies for oversight and to directly report complaints to. And it can’t be lost in these small victories the roadmap to laissez-faire exploitation being replicated elsewhere by markets in their initial stages. Ad hoc industry measures are not a permanent solution. But in spite of cultural, regulatory and technological differences, the improving digital lending markets in Kenya, India and Indonesia through private sector measures provide hope for a more responsible future than the industry’s initial phases suggest.

Image courtesy of Konstantin Evdokimov

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

Africa’s VC Boom: An Enabling Present or a Bet On The Future?

Blockchain’s Emerging Opportunities in Emerging Markets