Three Fintech Trends From 2023 — And How They May Look In 2024

~7 min read

In 2023, the dichotomy between success and failure in the fintech world never felt more stark. Emerging technologies and protocols offered glimpses of fintech' future for frictionless, inclusive and secure financial services. At the same time, a diminished investment climate and certain unicorns gone bust put a damper on growth and extinguished hopes for simply exponential growth across the sector. This mixed bag of dashed hopes and groundbreaking innovations signal the transition into a new stage in fintech’s development — one of skeptical investors on the one hand, but also product maturation and progression on the other. In the context of that muddled picture, let’s highlight some of 2023’s most important developments, taking a look at how Mondato Insight covered these topics — with a brief look at how these trends may fare in 2024.

1. The Rise of Generative AI

If there was one trend to define 2023, it would certainly be the advent of generative AI technology. Mondato Insight opened the year discussing the challenges and opportunities that ChatGPT would provide to the fintech sector. At that exciting juncture, it was mostly speculative the expected transformative impact ChatGPT would have — forecasting back then that such technology would overhaul customer service tasks to be automated yet reliable, slashing costs while better servicing customers, along with changing the game on fraud and product personalization.

In February, Mondato Insight went further in the AI discussion through an in-depth exploration of the meat-and-bones foundation fueling this AI revolution: synthetic data. Applications of synthetic data — like the generative AI models underpinning chatbots like ChatGPT, Bard and Q — have been what’s captured the public’s attention with its language processing capabilities, but it is the privacy-enhancing and machine-learning potential that synthetic data possesses that promises to transform financial services in the coming years.

Until now, financial service providers struggled to solve consumer data’s privacy-utility dilemma: the more useful data is for unearthing granular insights, developing tailored products and servicing customers, the more difficult it is to protect consumer data privacy. But synthetic data — while indeed potentially opening a pandora’s box of for fraudsters — is primed to be what fuels algorithms of the future spanning the operations of digital financial services from customer intake to personalized products and terms.

Source: Mostly AI

Source: Mostly AI

“Synthetic data generation technology can be used to automatically learn the patterns and correlations that are present in a data set to then create a completely separate data set. From a statistical point of view, you have nearly the exact same information. You would see similar insights like the same spending behaviors across micro segments. But you don't have any one-to-one relationship between a synthetic individual and your real customers.”

Alexandra Ebert, Chief Trust Officer, Mostly AI

Since then, AI has taken off across tech spaces, becoming an investment hit in an otherwise down year. Nearly all (99%) of financial services companies surveyed by Ernst & Young last month said they were using artificial intelligence in at least some form, with all saying they were using or planning to use generative AI in their operations.

What's next: Therein lies the tantalizing prospect — the infinite possibilities (good and bad) that can be realized through generative AI. There will be far more to cover in the months ahead at Mondato Insight on this topic, but if ChatGPT and its competitors were what grabbed the headlines in 2023, synthetic data and its applications will have even greater long-term implications that will only increase in importance over time — if in not such a front-facing manner.

The trickledown effects on this transition in data storage, capture and usage will be manifold, such as further accelerating the transition away from third-party data source mining and towards customer data ownership regimes, which may actually benefit industry leaders in an increasingly API-enabled, BaaS-driven world.

2. Integrating Corridors

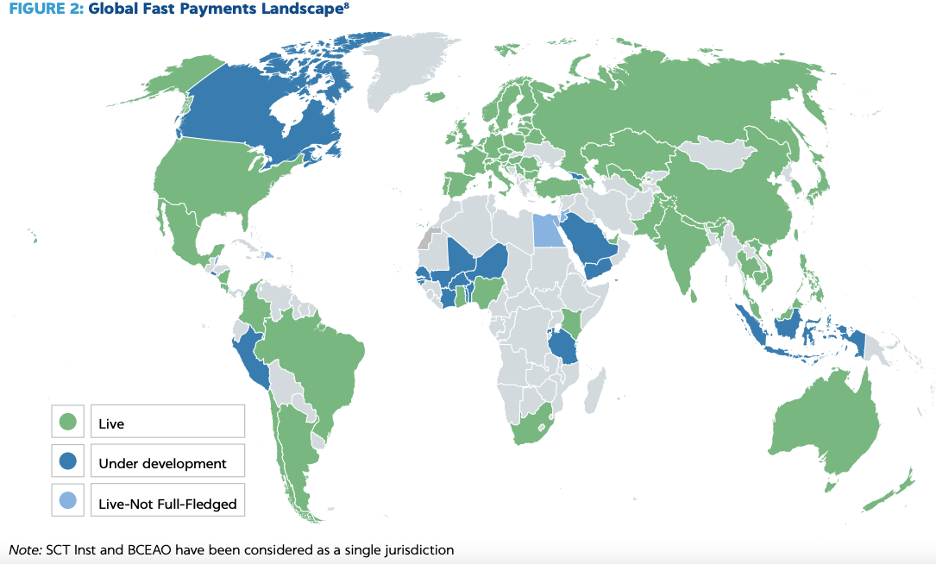

Likewise, 2023 marked a time of remarkable expansion in inclusion and access, often through improvements in standardization and, especially, instant payment regimes. Early successes like Brazil’s Pix affirmed the need to create instant payment rails that are treated as a public good, which can serve as the infrastructure for further protocols and innovations by private sector players. After earlier, private sector-driven schemes often failed to enable consumer adoption, a recent World Bank survey found that over 75% of instant payment schemes were now driven by the central bank or governmental agencies.

Now, we are starting to see instant payment schemes — and the ecosystem of protocols and services it can be the foundation for — proliferate across the world, including both underserved populations and, as Mondato Insight discussed this past year — underserved markets.

Source: World Bank

Source: World Bank

Mondato Insight discussed in 2023 instant payments schemes’ increasing role in driving up digital financial technologies’ usage that for years lagged far behind financial access figures. 2023 saw India continue to take tremendous strides in its efforts to digitize, exemplified by the multiplying successes emanating from its United Payments Interface (UPI) system, which is now the bedrock for an entire ecosystem of digital finance.

Mondato Insight also described this past year the transformation taking place integrating global corridors and making cross-borders frictionless. In Africa, regional integrations like PAPSS have continued to grow, but unsteadily, facing barriers to entry within some jurisdictions. Mondato Insight detailed the fits and starts of implementing such systems in places like the East Congo, where mobile money operators like Airtel and Orange as well as local fintech companies, are implementing the technical integration of local systems through back-end providers like MFI Africa.

These advances come as the ISO 20022 standardization protocol — a key element to making a near zero-cost, cross-border, instant payment network possible — continues to see increasing adoption, with adoption rates by central banks more than doubling in the past year.

What’s next: The immense benefits provided to consumers, financial service companies and regulators in fostering such standardization and integration is bound to continue apace. This will be especially important as the fintech revolution extends beyond now-saturated, larger markets towards smaller markets with narrower margins of errors for fledgling digital financial service companies.

As Mondato Insight detailed this past year, issues achieving sustainable economies of scale has been a major deterrent for digital financial services to take root in tiny markets. Squabbling governments of smaller countries have impeded efforts to better integrate markets and regional rails, with Mondato Insight coming across such issues in locales as varied as West Africa and the Caribbean this past year. But stakeholders on the ground in these places see cross-border integration as the only sustainable path forward — and one likely to be pushed by leading telcos hungry to tap into new markets at greater efficiencies.

3. Resilience and Disappearance

For all the possibilities and inexorable progress that fintech evinces, 2023 was the year that companies had to tighten their belts, toss away appealing to the eye yet ultimately unsustainable business models, and even settle for down rounds. Prolonged inflation, subsequent rises in interest rates and implosions from once-digital finance darlings set the stage for a brave new world for forward-thinking digital finance models struggling with narrow or nonexistent margins.

Mondato Insight explored these dynamics through the prism of digital banks in emerging markets this past year. Facing less competition, digital banks in emerging markets showed themselves often to be more resilient than their developed market counterparts in acquiring sufficient market shares while maintaining lean operations in already high-interest rate environments.

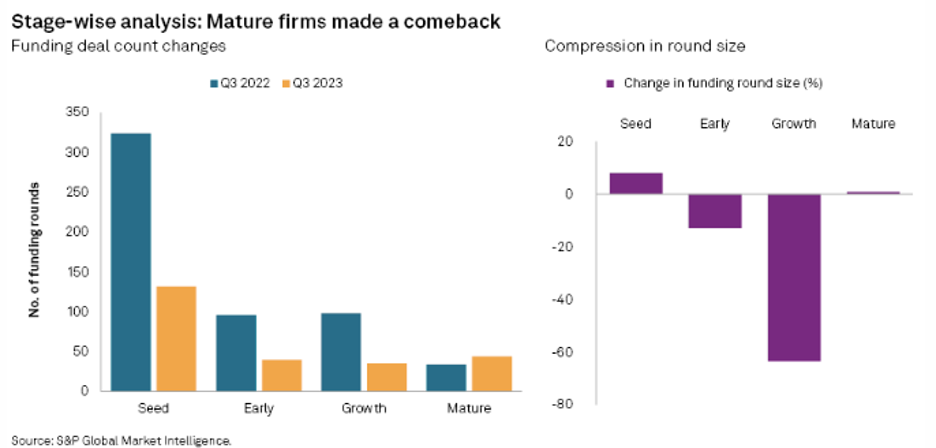

Even with certain bright spots, the latest funding numbers from Q3 highlight how difficult this past year was, though, especially for early-stage companies struggling to break past the valley of death. The latest Q3 figures from S&P Global revealed a 36% drop in VC funding towards fintech compared to Q3 a year before. The first nine months of 2023 total saw $29 billion in fintech investments compared to $54 billion in that same time span the previous year.

Source: S&P Global

Source: S&P Global

What’s next: Though a return to 2020’s free-for-all bonanza is not in the cards, the worst is likely behind us. Inflation is abating especially in more advanced economies, with experts expecting some central banks to begin cutting borrowing rates again by the middle of 2024. Late-stage companies, by contrast, managed to achieve a funding increase year-over-year in Q3, providing more evidence that relatively few proverbial front-runners have the upper hand in this environment.

Combined with deeper integrations through standardized protocols and developing instant payment schemes — all of which benefit the synergistic network effects that platforms seek to foster — these dynamics suggest 2024 may be a particularly fruitful year for consolidation, as tech titans solidify their grip on markets. Even regionally speaking, investors are heading for the most attractive jurisdictions, with the U.S., UK, India and Singapore accounting for more than half of founding rounds in Q3, according to S&P.

And when it comes to the primary winner of 2023’s funding rounds — AI-oriented fintech plays — all bets are off, as innovation proliferates in new markets and industry leaders double down on staying ahead of the pack.

Transitioning to a New Year

Amid these at times divergent or contradictory trends, the theme of the moment can be best boiled down to that of transition — a once-nascent sector now spreading its wings, facing threats as it hadn’t before while finding itself embraced and integrated as a ubiquitous function of daily life.

Entering 2024, we now find ourselves in a world where the fintech revolution has reached all corners of the globe, even the most remote or foreboding parts. That, most importantly, will continue to accelerate. Turbulence and chaos aren’t leaving entirely, but this upcoming year may offer another step change in how businesses, governments, and people engage with digital financial technologies and services.

Image courtesy of Kajetan Sumila

Click here to subscribe and receive a weekly Mondato Insight directly to your inbox.

Gen AI In Emerging Markets: Is The Hype Warranted?

Sanctions And CFT: Recent Palestinian And Russian Case Studies